Module 12: Emergency Management Cycle for Coastal Hazards

Module 12: Emergency Management Cycle for Coastal Hazards

Introduction

We have demonstrated in previous modules just how destructive coastal hazards like storm surges and tsunamis can be. In Module 11 we focused on the vulnerability of coastal communities around the world to tsunamis and storm surges. In Module 12 we will explore the four stages of the emergency management cycle – mitigation, preparedness, response, and recovery – and examine policies related to tsunami and storm surge impacts.

Ever-greater numbers of people are migrating to coastal areas, thereby increasing exposure to these hazards. Consider these statistics – from Gaul, 2019.

- Population: In 1940 the population of the Atlantic and Gulf coasts of the U.S. was 16 million. In 2017, it was 70 million. That is more than a four-fold increase (Gaul, 2019).

- The costs of hurricane damage have escalated over recent decades as population density has increased along the coastlines of the U.S. In the past 20 years, coastal storms have cost $750 billion in damages. This is a six-fold increase from the prior two decades (Gaul, 2019).

- Seventeen of the most expensive hurricanes occurred since 2000.

- A warming ocean is fueling more intense storms, which in turn is leading to greater costs in terms of damage and human suffering.

These trends are likely to continue into the future. So the problems we have witnessed in our favorite coastal cities along the U.S. coastline in the past couple of decades are likely to increase in magnitude as the oceans warm and rise and the population of coastal cities continues to grow.

Meanwhile, over half of the United States' economic productivity is centered in the coastal zones, and almost all of these areas are vulnerable to storm surge or tsunami. Airports, too, are vulnerable: the U.S. National Climate Assessment reports that 12 of the 47 largest airports in the United States are vulnerable to storm surge hazards. During Superstorm Sandy, all three major New York area airports – LaGuardia, JFK, and Newark, NJ – experienced storm surges of up to 14 feet. The Pentagon is also well aware of the threat of sea level rise. The Naval Station in Norfolk, Virginia floods over ten times a year, a trend that will certainly get worse.

Sound coastal emergency management policies can reduce the vulnerability of residents to coastal hazards. In the case of tsunami policy, the United States is a world leader, with the nation’s public policy initiatives significantly reducing tsunami vulnerability in the United States and across the world. Coastal communities around the U.S. have recently experienced frequent and devastating flooding from storm surge. Policy addressing vulnerability to this type of coastal hazard may not be keeping pace with the climate factors behind these events. We will consider this dilemma in Module 12, among other policy questions.

After exploring the stages of the emergency management cycle, we will visit several case studies to better understand how the emergency management cycle works in real examples and to determine how policies may be improved as the threat of coastal hazards and disasters increase.

Goals and Objectives

Goals and Objectives

Goal

Students will assess how government and stakeholders can plan for and respond to coastal hazards.

Learning Objectives

By the end of this module, students should be able to:

-

examine the stages of the disaster management cycle and its application;

-

identify and compare policy options for preparing for and responding to immediate coastal hazards;

-

critically assess the implementation of the emergency management cycle in real disaster case studies.

Module 12 Roadmap

| -- | Assignment |

|---|---|

| To Read |

|

| To Do |

|

Questions?

If you have any questions, please use the Canvas email tool to contact the instructor.

Policy, Natural Hazards, Disasters, and the Emergency Management Cycle

Policy, Natural Hazards, Disasters, and the Emergency Management Cycle

Let’s go over some emergency management terminology to begin.

Policy

A policy is a principle or set of principles that guides decisions and tries to produce sensible, positive outcomes or to avoid the negative effects of some behaviors. A policy can apply to governments, businesses, other groups (such as sports teams or college courses), and even individuals. Policies are often established by governing bodies and implemented by executive officers. Many levels of government, schools, etc., have recently developed policies to help guide people through the COVID-19 pandemic.

Policies can only suggest ways for people or groups to do the right things or to avoid doing the wrong things, while rules or laws can use punishment as enforcement. We have all become familiar with the heated debates about mask-wearing during the pandemic. These arguments underline the difference between policy and rule of law.

So, tsunami and hurricane storm surge policies aim to help the public avoid or minimize harm from these natural hazards and recover quickly and efficiently from them when they strike.

Natural Hazards

Natural hazards are geophysical events that pose threats to human life or health, to the natural or built environment on which people rely for life support, and to things that people value, such as economic wealth or material possessions. Natural hazards are potentialities; that is, they have not yet happened but could occur at some time in the future.

Disasters

When a natural hazard such as a tsunami or hurricane does become active, it can trigger a disaster. Natural disasters are the major adverse human events resulting from natural hazards. Disasters are typically associated with loss of life, impaired human health, destruction of the natural and built environment, financial damage, and loss of land and possessions. The severity of the disaster is a function of the magnitude of the geophysical event coupled with the vulnerability of the people and place, which was the topic of Module 11.

Emergency Management Cycle

The emergency management cycle is used to understand appropriate human preparation for, and response to, disasters, including those resulting from a coastal hazard. The emergency management cycle can be divided into four stages: mitigation, preparedness, response, and recovery.

Mitigation

Mitigation includes all efforts that a person, household, community, or any other social unit takes to make a disaster less likely to happen or to reduce the negative effects if a natural hazard were to occur. Mitigation activities occur well before a natural hazard strikes and can be structural, such as building a sea wall, or non-structural, such as developing a warning system.

Preparedness

Preparedness, in contrast to mitigation, can take place right before the natural hazard strikes. Its goal is to make sure that the individual or community knows which tools to possess and how to use those tools, what actions to undertake. The actions can also continue during the hazardous event, or immediately after disaster strikes. In preparing for a hurricane, for instance, important preparedness activities may include planning for evacuation, including knowing when to evacuate, which destination to evacuate to, and what evacuation route to take.

Response

Response is the emergency assistance that takes place during or immediately after a disaster. Its purpose is to save lives, treat injuries, and reduce property damage while meeting the most fundamental needs — water, food, shelter, and medical aid — of the people affected by the event. The response period is stressful both to emergency managers, who face limited time, information, and resources, and to the public, who face evacuation, family separation, and the loss of property and loved ones.

Recovery

Recovery is the stage during which individuals, families, communities, and governments repair and reconstruct what has been damaged by or lost in the disaster. At the same time, recovery presents an opportunity to reduce the risk of a similar catastrophe in the future – in other words, to start mitigation activities and thereby start the emergency management cycle again.

In reaction to the disaster, governments usually provide substantial resources for recovery, including economic recovery, housing recovery, and individual, family, and social recovery, and possible mitigation of potential future natural hazard events. In addition, funds and assistance come from many other sources, including non-profit organizations, faith-based organizations, and volunteers.

Mitigation

Mitigation

Introduction

Mitigation involves taking action to reduce risk. Mitigation is a long-term planning activity, unlike preparedness, response, and recovery, which are more immediately part of the emergency itself. But mitigation can begin following a disaster, during recovery, to mitigate the effects of any future disaster. In the mitigation phase of the emergency management cycle, activities aimed at decreasing the likelihood of disaster or reducing its negative impacts can either be structural or non-structural. Examples of structural mitigation activities include building physical infrastructure such as sea walls or retrofitting existing buildings to withstand the hazard, or to serve as shelters. Instances of non-structural mitigation activities include developing storm surge warning systems, post-disaster recovery plans, and educational programs. Other non-structural mitigation measures include flood insurance programs (although some consider this as part of preparedness), and land use planning activities like zoning. As you can see, mitigation activities are wide-ranging and can overlap with other phases of the emergency management cycle.

Learning Check Point

Please take a few minutes to think about what you just learned and answer the question below.

Structural Mitigation

Structural Mitigation

Constructing levees and seawalls is probably the most obvious mitigation measure to protect a community against disaster. Seawalls can be very effective in physically impeding the progress of a tsunami and are common in tsunami-prone parts of the world, such as Japan. However, as the case of the Fukushima Daiichi disaster, which we covered in Module 11) demonstrates, cost considerations or inaccurate estimates of potential tsunami heights may result in seawalls of insufficient height to serve their intended purpose. Additionally, structures like levees require maintenance, and it was a lack of attention to the structural integrity of the levees protecting New Orleans that lead to the disaster of Katrina’s flood there.

In Module 8, we looked at the various hard structures and their designs for protecting coastlines and communities. In Module 10 we looked at smart building measures – both traditional and newly innovative. These measures are all methods for mitigation, and many have been used for centuries. The managed retreat strategies we explored in Module 9 are also considered mitigation measures.

Another structural mitigation measure is constructing or retrofitting buildings for use as shelters. As hurricane storm-surge risk zones expand as sea levels rise, so the location of existing shelters in hurricane-prone regions must be reevaluated over time. It is also important to note that tsunami shelters are only useful if a community is far enough from the tsunami source to allow sufficient warning for residents to get to the shelter. On the northeastern coast of Japan, for example, residents may have only minutes to respond between the time of the earthquake and the arrival of the tsunami.

Non-Structural Mitigation

Non-structural Mitigation

Warning Systems and Community Education

Developing effective warning systems is an essential non-structural mitigation activity. Hurricane forecasts typically provide a few days’ advance notice of the potential for a hurricane affecting a particular area; While not perfect, storm surge forecasts can provide enough time for emergency managers to issue warnings. After Superstorm Sandy, a storm surge warning system was developed for the Meadowlands District in New Jersey that can provide storm surge forecast maps at least three hours in advance. When a hurricane is approaching the shoreline of the U.S. the National Hurricane Center issues regular advisories which give graphic information about storm surge, as well as estimates of the height of the storm surge for an area (form of estimates for certain stretches of coastline). Local authorities can take this information and use it to warn residents, for example, if a certain roadway is likely to flood, or if a levee is likely to be topped. Each storm is unique and, due to the many factors driving the impacts in a particular location (say, your house), storm surge forecasting is still tricky to predict on a small scale, especially because it is affected by even small changes in the landfall location as was the case in Hurricane Laura in August 2020. On a neighborhood or larger scale, the National Storm Surge Hazard Maps [9] provide an interactive mapping tool to estimate storm surge based on the hurricane category on the Saffir-Simpson Scale.

Establishing detection and warning systems are particularly essential to tsunami policy, as we have mentioned in previous modules. After a 1946 tsunami killed 160 people in Hilo, Hawaii, and 5 in Alaska, the United States established its first tsunami warning center in Ewa Beach, Hawaii. This center, now known as the Pacific Tsunami Warning Center (PTWC), is responsible for issuing most tsunami warnings for areas bordering the Pacific Ocean. A center in Palmer, Alaska, currently known as the National Tsunami Warning Center, provides warnings for Alaska, the Pacific coast of Canada, and the Pacific coast of the continental United States.

Following the 2004 Indian Ocean tsunami, which cost hundreds of thousands of people their lives, the United States spearheaded an effort to establish regional warning systems worldwide for coastal regions vulnerable to tsunamis. Initial responsibility for managing the Indian Ocean and Caribbean Sea systems fell to the PTWC, but the Indian Ocean system is now administered by national government organizations in Australia, India, and Indonesia, while a Caribbean Sea center opens in Puerto Rico in early 2021. Together with the North Atlantic and Mediterranean Tsunami Warning System, a European partnership, these organizations provide critical early warnings for tsunami events that serve an important preparedness function for regions exposed to tsunamis. See more details about the Global Tsunami Warning and Mitigation System in the Banda Aceh Case Study in this module.

In addition to having a sophisticated warning system in place and multiple ways to communicate warnings to residents, including phone texts, email, local TV news, as well as announcements via other broadcasting methods such as mosque loudspeakers in Islamic communities, and community group messenger networks, public education about what to do when an alert is broadcast is essential. This need is articulated in the case study in this module on the 2004 Indian Ocean tsunami and its impacts in Banda Aceh, Indonesia.

Other Non-Structural Mitigation Activities

Post-Disaster Recovery Plan

After disasters occur, the recovery process can be complex and overwhelming, so a post-disaster recovery plan is another helpful non-structural mitigation measure put in place by community-level government agencies. There are many aspects of recovery – economic, housing, environment, and social recovery – that should be considered. There are also many stakeholders who need to be involved in the recovery process. Developing a post-disaster recovery plan can identify and prioritize tasks and can recognize and engage stakeholders before an event takes place, thereby assisting recovery and minimizing chaos during a stressful time.

Zoning

Another non-structural mitigation measure is zoning. Zoning enables local or regional governments to set restrictions on the types of structures that can be built in various locations within their jurisdictions. This tool can be used to prevent critical infrastructures such as power plants and hospitals from being built in tsunami or storm surge inundation risk zones. It can also be used in conjunction with development restrictions to prevent projects that would damage natural habitats, such as mangroves, that can mitigate tsunami or hurricane damage.

Education and Outreach

As we noted above, educating the public about mitigation measures are essential so that residents know what they can do to protect themselves, their families, and their property. So, education about tsunami and storm surge planning can fall under mitigation, but it is also part of preparedness.

Mitigation Summary

Mitigation Summary

Policies that promote mitigation are crucial to reducing the threat of disaster caused by natural hazards. In the United States, the National Tsunami Hazard Mitigation Program (NTHMP), run by NOAA in cooperation with USGS, FEMA, and the coastal U.S. states, has been developed to encourage tsunami mitigation practices. For more information, see the Tsunami Risk Reduction for the United States: A Framework for Action [14]. NOAA also manages the Storm Ready [15] and Tsunami Ready [16] programs, which recognize thousands of counties, communities, universities, and other members that meet a set of mitigation and preparedness criteria. Such programs and the policies advancing them are foundational to protecting people and places from disaster.

Preparedness

Preparedness

The goal of the preparedness stage of the disaster management cycle is to enhance people's capacity to respond to natural hazards and recover from a disaster. The basis of preparedness is planning, whether that planning takes place at the household, local, state, national, or international level. Thus, policies from a local to international scale that guide sound hazard and disaster planning are essential. Emergency planning and communication of plans for their successful execution when a hazard occurs, happens at many levels of society, from the federal level down to the individual. Therefore, for organizational units including state, county, and city governments, to schools, universities, hospitals, and many other organizations, a clear plan is essential.

Insurance Challenges

Insurance Challenges

Insurance coverage for homeowners in hurricane prone areas is becoming one a major policy challenge. As it turns out both instructors have their own insuance nightmare stories to tell.

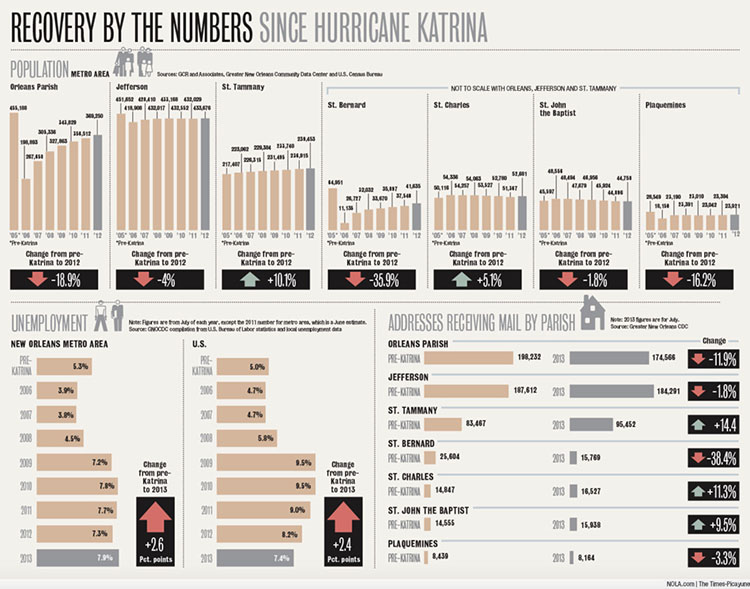

The recent and ongoing cost increases for homeowner’s and flood insurance coverage in coastal Louisiana (including metro New Orleans), coupled with collapse or relocation of some insurance companies, is negatively impacting ordinary, working people who live in the area. Dinah’s experience may be “average” compared to her neighbors, some of whom have suffered much greater heartache and loss following Hurricane Ida in 2021. Ida hit the Louisiana coast as a category 4 storm, wrecking the Gulf town of Grand Isle and leaving a wide swath of flooding and wind damage in its wake as it traveled inland. Jogging close to New Orleans, it wreaked havoc in the western suburbs of the city, leaving tens of thousands of damaged roofs, not to mention cutting power and water for weeks. Then came the insurance nightmares, playing out over the next couple of years. Dinah had a homeowner’s policy with a company that left Louisiana because of Ida’s losses. Although this insurance company did cover the cost of the repairs, including a new roof, a new homeowner’s policy had to be found. As of 2023, the cost of the new homeowner’s policy is approximately 3 times the cost of the original one at over $3,000 annually. Many families cannot afford these policies, and some go without. This results in neighborhoods sporting blue tarps for years after a storm as repairs are unaffordable for many families.

Meanwhile, flood insurance has increased steadily each year (FEMA's updated Risk Rating 2.0 is allowed to impose an 18% annual increase to existing policies). Dinah’s house is in flood zone X and does not require a flood insurance policy, but recent experiences in Louisiana mean it is wise to carry flood insurance in this location. The house is a few blocks from the Mississippi River levee and close to much lower ground and flood zone AE. Dinah’s family also has a small home in coastal Mississippi (flood zone AE), built recently and elevated to 20 feet (3 feet above the required base flood elevation). Flood insurance on this property under the new National Flood Insurance Policy is $4,000 annually. Again, this is a modest house and built with flood mitigation in mind. Other properties are much more costly to insure or are uninsurable because they do not meet minimum elevation requirements. In some cases, families use cash to purchase homes and go without insurance. It is clear as Dinah looks around and talks to neighbors that these increasing costs are having a deep impact on the housing market, changing what were previously modest neighborhoods in coastal areas into places only the wealthy can afford, and many properties are bought by companies that make rental money from them. This is happening all around the coastal areas of the U.S. and impacting millions of people.

Tim’s insurance nightmare started after hurricane Fran sent a 150 foot red oak tree onto his Chapel Hill house at 2AM on September 6th 1996. The tree caused extensive roof damage and water damage in the house. Ceilings were wrecked and carpet was damaged. He contacted his insurance companies, one of the largest insurance companies in the country, and they came out to the house within days and promised to help restore the damage. It was a shock when a letter from the adjustor arrived with estimates of what the company would pay. 54 cents a square foot for ceilings to be repaired, a few hundreds of dollars for the roof. This was insult to injury for Tim and his family who had endured to trauma of a massive tree hitting their roof followed by 10 days without power in sweltering heat.

This anecdote is sadly very common for home and business owners who have been impacted by storm damage and the situation seems to be getting worse as coastal areas have become increasingly developed and storms more devastating. In fact, insurance companies themselves have been faced with major financial losses resulting from major hurricanes. Homeowners’ premiums have risen sharply, and in several cases, insurance companies have left states such as Florida and Louisiana because business is not profitable. This leaves states in a real bind as these two videos show.

Video: Florida Faces Insurance Crisis From Hurricane Ian (7:56)

Video: Louisiana's Insurance Crisis: Homeowner's policy rates by ZIP Code (7:22)

The National Flood Insurance Policy (NFIP)

The National Flood Insurance Program (NFIP)

If you purchase property in a flood zone, and you have a mortgage, you are required to purchase a flood insurance policy in addition to a homeowner’s policy. The National Flood Insurance Program, (NFIP) was created by legislation in 1968 and has maintained the affordability of insurance for homeowners in flood-prone (both inland and coastal) areas since then. This sounds like a great idea on the surface, but there are some problems with this policy that need to be addressed by Congress.

The NFIP was created to protect property owners in flood-prone areas from disastrous losses in the event of flooding. NFIP, which is managed by the Federal Emergency Management Administration (FEMA) is federally subsidized and kept affordable by borrowing money from the U.S. Treasury in order to keep the program solvent. It is currently in “deep water” so to speak, in fact, it is in debt to the tune of $40 billion. Climate change is complicating the picture. Because of the increase in the frequency of catastrophic flooding in the past 20 years, NFIP has become deeper in debt and in danger of lapsing coverage for property owners. For example, in 2017, many Houston residents whose property flooded in Harvey were not required to have insurance based on their flood zones. This raises further questions about how to manage flood loss in the coming years. The NFIP is no longer a sustainable way to protect property, and it is clear that changes are needed.

Also, although it was not originally intended to do so, the affordability of flood insurance through the NFIP has encouraged development in flood-prone areas, creating an even bigger problem. Homeowners have become accustomed to the availability of affordable flood insurance for their primary residences as well as their second homes on the coast, the number of which has ballooned since the NFIP first came into existence. According to a 2013 study, about one-third of all properties insured under NFIP are second homes (Gaul, 2019).

Without government subsidies insurance rates are likely to increase dramatically, so attempts to change the NFIP have so far been unsuccessful. However, FEMA is in the process of updating the NFIP with the Risk Rating 2.0 Program, which went into effect in 2021.

The overhaul is designed to help address some of the inequity issues with the NFIP and to update the process using current data and technology. New maps are replacing the older FIRM maps and properties are assessed based on their proximity to a water body as well as other features of the property. Raising your property’s height to an additional elevation above the standard base flood elevation* no longer reduces flood insurance premiums, however. You can read about these changes at FEMA: RiskRating 2.0: Equity in Action [21].

The 21st-century rating system, Risk Rating 2.0—Equity in Action, provides actuarially sound rates that are equitable and easy to understand. It transforms a pricing methodology that has not been updated in 50 years by leveraging improved technology and FEMA’s enhanced understanding of flood risk. (fema.gov)

Video: Defining a Property’s Unique Flood Risk (1:15)

However, there is still work to be done, as in some cases flood insurance has become unaffordable. Lower-income families are having to forego insurance, placing them further at risk. The changes have the potential to change where people choose to build or buy, and the changes are also affecting the livelihood of people who live and work in communities that are flood-prone.

According to the Natural Resource Defense Council (NRDC) in It’s Time to Fix Our Water-Logged National Flood Insurance Program (nrdc.org) [24]:

Congress must act to create a means-tested flood insurance option that helps lower-income families purchase flood insurance, and that prioritizes those same families for flood adaptation assistance. (nrdc.org)

More on Flood Insurance Rate Maps and Base Flood Elevation

Flood Insurance Rate Maps | FEMA Flood Maps Explained [26] are used to determine a property’s flood insurance. A potential homeowner can access these maps before deciding to purchase property in a flood zone. The maps are also designed to help residents of coastal communities plan for and mitigate the flood risk to their properties by delineating flood zones and identifying Base Flood Elevations (BFE). The BFE is the height to which a location has a 1% annual chance of being flooded. A house must be built at or above the BFE to be eligible for flood insurance.

The FIRM zones are based on elevation and proximity to water, as well as several other factors that determine a property’s risk of flooding. Visit this site to read about the flood zones shown on a Flood Insurance Rate Map (FIRM) [27].

Emergency Operation Plans

Emergency Operation Plans

For state and local governments as well as entities such as hospitals, universities, and school districts, developing Emergency Operation Plans (EOPs) is a vital task. An EOP helps everyone who is involved in the disaster management cycle know what he or she should do from the point at which a natural hazard threatens to strike, all the way to the final recovery from the ensuing disaster. It explains who will do what, when, with what resources, and by what authority. Included in these responsibilities is the need to transmit hazard preparedness information and last-minute hazard information to the public. In the response period, when time is in short supply and everyone – from the highest government official to individual householders – is under stress, an EOP helps people respond appropriately and use resources efficiently. See an example of part of an EOP in Box 1.

Box 1: An example of an Emergency Operation Plans (EOP)

Brunswick County is located on the Atlantic coast of North Carolina and is often assaulted by hurricanes. It suffered several direct hits from hurricanes in the 1990s and most recently received a direct strike from category 2 Hurricane Arthur in July 2014. In response to this annual threat, the county in 2008 developed a long and detailed Emergency Operations Plan (EOP) for multiple hazards, including an annex designed specifically for hurricanes.

Presented here are modified excerpts of the hurricane annex to help you understand what an EOP looks like. The first part of this example defines Operating Conditions, or OPCONs, that trigger emergency management actions. There are 5 OPCONs: OPCON 5, Hurricane Season; OPCON 4, Alert; OPCON 3, Stand-by; OPCON 2, Preparation; and OPCON 1, Evacuation. The second part of the example lists important actions to take during the OPCON 2 Preparation phase.

OPERATING CONDITIONS (OPCONs)

The Control and Support Groups will be located in the Brunswick County Emergency Operations Center (EOC) at the Brunswick County Government Center. In the event that it becomes necessary to move the groups to an alternate EOC, the new location will be announced.

OPCON Triggers: To ensure that all activated personnel in the county have a coordinated hurricane response activities approach, the following OPCON levels will be utilized throughout the event.

- OPCON 5: Hurricane Season

This OPCON indicates that hurricane season is open. Brunswick County will stay at OPCON 5 as of June 1st, the start of the hurricane season. At this time, all hurricane plans and procedures should be reviewed. Alert Rosters should be updated and verified. Storms will be monitored and tracked at this level. - OPCON 4: Alert

If the Brunswick County Emergency Management Director determines that a storm could possibly threaten Brunswick County, the County will be moved to OPCON 4. The primary events that will take place at this level are the notification of key personnel of the threat, and initiation of preparatory activities. The EOC (Emergency Operation Center) will not be activated at this stage. - OPCON 3: Stand-By

Once the Brunswick County Emergency Management Director has sufficient information that a storm poses a significant threat, the County will move to OPCON 3. This decision will be based on each of the storm’s specific characteristics. The EOC will be activated at this level, either at a partial or full status. The primary events that will occur include discussing evacuation and conducting pre-evacuation conferences and other preparatory activities. - OPCON 2: Preparation

Once a decision is made to recommend a Voluntary Evacuation or Mandatory Evacuation, the OPCON level will automatically move to OPCON 2. The EOC will be under Full Activation at this level. At this level, shelters will be prepared for opening. Public notification will be coordinated and press conferences coordinated. It is understood that once the County moves to OPCON 2, the County is prepared to commit substantial amounts of money and resources to the effort. - OPCON 1: Evacuation

Once a Voluntary Evacuation or Mandatory Evacuation order is announced to the public, the OPCON automatically moves to OPCON 1. At this level, the primary activity will be the evacuation of the vulnerable population. The EOC will remain at full activation throughout the evacuation and landfall.

EMERGENCY SERVICES

- Manage the EOC Operations in accordance with the Brunswick County EOP.

- Notify the following agencies of the current situation:

a. EOC Operations Personnel

b. North Carolina Emergency Management EOC

c. National Weather Service, Wilmington

d. County Administration / Elected Officials

e. Municipalities

f. Utilities and other stakeholders

g. Adjoining County Emergency Management Divisions - Monitor the weather situation.

- Be available for media interviews and press conferences.

- Install Variable Message Signs at designated locations.

- Begin monitoring traffic patterns and prepare to adjust traffic signals, as appropriate.

- Prepare to implement the traffic assistance plan.

- Complete the establishment of the Amateur Radio Network.

- Position equipment to support evacuation.

- Take appropriate actions to protect critical Brunswick County facilities.

- Coordinate for the movement and/or protection of Fire/EMS equipment during the storm’s impact.

- Assist with status information concerning Law Enforcement Management.

- Prepare to open shelters.

- Coordinate with the PIO for a press release once the evacuation decision is announced.

- Prepare to open Special Medical Needs Shelters if needed. Coordinate with the PIO for a press release once the evacuation decision is announced.

- Position resources to assist with the management of the evacuation traffic. Resources must be in place prior to the start of the voluntary relocation.

- Prepare to conduct “evacuation warning” in the evacuation zones, within the unincorporated portions of the county.

- Implement the security plan in the evacuated areas.

Educating the Public about Tsunami and Storm Surge Preparedness and Warning Systems

Educating the Public about Tsunami and Storm Surge Preparedness and Warning Systems

Educating the public about the existence of warning systems, how they work, and how to react when it is activated are essential components of the preparation.

Tsunami Warning and Public Readiness

In the parts of the United States' most vulnerable to tsunamis – that is, the coastal zones of Hawaii, Alaska, Washington, Oregon, and California – this primarily takes the form of evacuation planning. Anyone driving through low-lying coastal areas of these states is likely to notice tsunami hazard zone and tsunami evacuation route signs lining the roads, and warning signs in beachside hotels and motels.

The National Weather Service’s Tsunami Ready [28]website provides a wealth of guidance for the public about what readiness for a tsunami involves and how to achieve it. Communities can organize tsunami ready training through the NWS program with the goal of achieving community-wide tsunami readiness.

Residents and visitors on the Oregon coast have several location-specific tools to use to learn about tsunami risk in their area and to receive messages about tsunami threats. The State of Oregon Department of Geology and Mineral Resources Oregon Tsunami Clearinghouse [29] is a web site where you can go to get detailed evacuation maps, smartphone apps to aid evacuation, and an interactive evacuation zone map viewer at NVS Tsunami Evacuation Zones [30].

Learning Check Point

Hurricane Storm Surge Warnings and Public Readiness

When a hurricane is approaching the United States and threatens to make landfall, Emergency Operation Plans go into action in the areas likely to be affected. As we mentioned above in the mitigation section, forecasting local storm surge levels can be challenging as it depends on several factors, including the track of the storm, exact landfall location, the timing of the tide cycle, water depth, and the angle and slope of the shoreline, complicating accurate predictions. This, in turn, affects preparation communication.

Therefore, hurricane preparation in a community that may receive a storm surge must start well before the magnitude of the threat is certain for that location. Evacuation orders should be made 72 hours in advance of a storm’s landfall. Many mandatory evacuations have been communicated to the public, only to see the path of the hurricane turn elsewhere. This means that city or county leaders must decide several days out to close schools and businesses, mobilize transportation for those without, prepare shelters, etc. Additionally, all communities within the “cone of uncertainty” of forecast tracks based on modeling, must be on alert and be making preparations. A storm’s track can change significantly during the approach, depending on the steering factors. Hurricane Sally in September 2020 is a good example. Greater New Orleans and Southeastern Louisiana were under a hurricane warning and evacuations and preparation well underway but within 36 hours of landfall, the track moved significantly to the east, so that Mississippi, Alabama, and western Florida received the brunt of the storm surge effects and hurricane warnings were downgraded to tropical storm warnings in New Orleans. Residents of the storm-aware Gulf coast must stay vigilant for these kinds of changes in the forecast.

On a family level, preparedness begins with making a hurricane supply kit (see below) and making a plan for the event of a hurricane. Within 72 hours of landfall, multitudes of decisions must be made, and actions taken. A very abbreviated list of things to be considered in a coastal community threatened by storm surge is: Securing or moving all moveable/ floatable items to a safe place; Securing boats in dock; fueling and moving vehicles, boats, trailers, etc. out of harm’s way; securing the house, by boarding up windows or closing hurricane shutters, and turning off water and power; planning evacuation route and accommodation while away; and communicating with neighbors and family members to ensure everyone has a way to evacuate and a place to go.

Information driving preparedness is broadcast in many ways. A resident in a storm surge zone can best track the storm via local TV news stations and weathercasts to find details about the storm’s impacts in their community. These are often pushed as notifications to mobile devices. The National Hurricane Center [31] provides many kinds of useful graphics that are updated every 4 hours. Mobile Apps are available to access this information too.

{kind=link}

Challenges with Communicating Emergency Plans

Challenges with Communicating Emergency Plans

It is easy to recognize the importance of communicating emergency plans to the public, but many problems can occur in the process. In reality, when emergency information is sent out by a city or state governmental entity, some people will not receive this information, or they may not respond appropriately to it. For example, if the information is broadcast only in English, then non-English speakers in the United States may not fully understand the messages. Poor households in developing countries may not have radios, televisions, smartphones, or other devices needed to receive the information.

Due to many factors (cultural, language, economic, psychological, and social), some people who do receive and understand the government’s communications will choose not to heed warnings and follow instructions given by the government. In the case of Hurricane Katrina, many long-time New Orleans residents chose to stay in New Orleans despite dire evacuation warnings. Among many reasons used for not evacuating, some included: financial constraints on their ability to evacuate the city (typically lack of transportation and no funds for traveling); frequency of hurricane evacuation warnings in recent years (evacuation fatigue); misconceptions about the severity of the storm; perceptions that they were not vulnerable to hurricane risks; worries about leaving pets; and concerns about the need to protect their property from criminal activity.

In many communities in the U.S. and elsewhere in the world, cross-cultural communication has been adopted to ensure all residents receive important messages for preparation for hazardous events. Cross-cultural communication recognizes the diversity of target populations in terms of language and culture, and emergency managers must take these factors into account so that messages are broadcast in the multiple languages spoken in the community in question. Using multiple media platforms and methods for disseminating messages is also essential. The technology available to many people such as texting and social media has helped greatly in recent years. Traditional media like television, radio, newspapers, the Internet, and printed flyers are still important, but other ways of communicating, such as through multiple social media platforms, have become more and more important. Modern communication tends to depend heavily on the mobile or cellular telephone network. In cyclone and tsunami conditions, communication towers can be toppled and rendered useless. In 2005, when cellphone use was common, but texting was less common, loss of communication was an enormous problem across the Gulf Coast following Hurricane Katrina, rendering cellphones useless and greatly hampering search and rescue and preventing people from locating loved ones.

Learning Check Point

Please take a minute to answer the question below. It will not be graded, but it may help you on the Module Summative Assessment.

Creating an Emergency Supply Kit

Creating an Emergency Supply Kit

The Department of Homeland Security’s website: Ready [34] gives guidance to Americans on readiness for all types of emergencies. The section focusing on hurricane preparedness includes this engaging video to catch the viewer’s attention.

Please watch the following short video on hurricane preparedness from Ready - Hurricanes [35].

Video: When the Waves Swell (1:30)

A basic emergency supply kit suggested by ready.gov includes the following recommended items to prepare in case of evacuation:

- Water, one gallon of water per person per day for at least three days, for drinking and sanitation

- Food, at least a three-day supply of non-perishable food

- Battery-powered or hand-crank radio and NOAA Weather Radio with tone alert and extra batteries for both

- Flashlight and extra batteries

- First aid kit

- Whistle to signal for help

- Dust mask to help filter contaminated air and plastic sheeting and duct tape to shelter-in-place

- Moist towelettes, garbage bags, and plastic ties for personal sanitation

- Wrench or pliers to turn off utilities

- Manual can opener

- Paper local maps

- Cell phone with chargers, inverter, or solar charger

I am adding a couple of items to this list from the article in the Tampa Bay Times linked below:

- Camping equipment – Sleeping bags, pillows, and propane stove

- Plenty of cash to tide you over a period of no power for digital payment transactions

- Prescription medications and medical records if health conditions warrant

- Personal documents such as government ID, passport, birth certificate (latter should be stored in a dry box in a safe place if not included in evacuation kit)

Emergency Supply List

Building an emergency supply kit is an important hurricane preparedness activity. Go to Ready [37] and find a document called Emergency Supply List. This is a list that helps you build an emergency supply kit. The document identifies recommended basic items and additional items for adding to the kit. Answer the questions below, identifying the items listed either as a “basic item” or an “additional item” based on this document.

Learning Check Point

Check all that apply for each question

Additional Emergency Preparation Considerations

Additional Emergency Preparation Considerations

Example of Community Hurricane Preparation – Tampa Bay Times

Tampa Bay Times provides readers with very thorough guidance on hurricane preparation:

- Hurricane 2019: The gear you need to stay safe - and comfortable - for the storm [5]

- Hurricane 2020: Protect your home, business, documents, and photos [38]

These two articles cover hurricane preparation – including protecting property and preparing for evacuation. The article covering protecting homes and businesses makes some very important points relevant to any hurricane season, but particularly relevant to 2020, with the extra complication of the COVID-19 pandemic. It emphasizes the importance of planning ahead and making preparations such as purchasing supplies for securing homes and businesses (generators, plywood, storage bins, etc.) early in the hurricane season, and not waiting until a storm threatens.

It also details important tips on storing important documents in waterproof containers ready for evacuation and having a supply of prescription medications on hand for the event of a long period without pharmacy service. The importance of these details may easily be overlooked until the event. Many New Orleanians can attest to this, having neglected to prepare ahead of time and protect essential documents like birth certificates and medical records, which had to be replaced after Katrina. Another really important tip is to have cash on hand. Without power, normal methods of card payment and bank ATM machines and the like do not work. Without cell phone service and power, the ability to access information and to do online banking and shopping is severely curtailed.

In addition, the importance of preparing digital copies of important documents cannot be overemphasized. But this also brings up the importance of taking care of computers and other digital devices and office equipment. File backup onto portable hard drives is essential and once this is completed, if a storm is threatening your area, desktop computers, larger devices, and machines should be powered down and unplugged. All valuables should be moved to the highest points of homes, such as upstairs, if possible. Tablets, phones, etc. should also be backed up but they should be included in the to-go list. It’s important to remember that although you hope you will be able to return in a couple of days after evacuation, this may not be possible. So, preparing for at least one week is important. After Hurricane Katrina, most New Orleans residents could not return for 6 weeks or longer and returned only to survey destroyed properties.

Learning Check Point

This activity will not be graded, but the Module Summative Assessment requires you to have the skills and knowledge it applies. Please take a few minutes to think about what you just learned and answer the questions below.

Summary: Preparedness

Summary: Preparedness

In short, policies that encourage emergency planning, including effective communication of warnings and evacuations, are foundational to protecting people and places from the ravages of tsunamis and hurricane storm surge.

Response

Response

Response policies guide actions undertaken during and in the immediate aftermath of a tsunami, storm surge, or other natural hazard events. The most immediate response is activating warning systems, evacuating residents, and activating the emergency plan (if there is one available). With sufficient warning time, it may also be possible to pre-position personnel and supplies that will be needed for recovery efforts in areas adjacent to those likely to be affected by the tsunami or storm surge.

Immediately following the passing of the hazard event, the scope of the disaster becomes evident, and response activities expand considerably. It is important for governmental staff and others to follow their assigned responsibilities according to the EOP. For emergency managers, the most urgent need is search and rescue. Locating victims and providing medical treatment needs to be accomplished as quickly as possible. Search and rescue teams also may be responsible for addressing dangerous conditions left in the aftermath of the disaster, such as dangling live wires and gas leaks. The emergency needs to be assessed and updated regularly as new information becomes available and the situation on the ground changes.

{kind=link}

Overcoming Response Challenges

Overcoming Response Challenges

While many people and organizations are eager to help in search and rescue activities, numerous challenges occur during this tense period. For example, volunteers from outside the area might have a hard time locating victims or knowing the most urgent needs of local people or communities. Using real-time tools can help address this issue. Disaster victims and other local people should be encouraged to use Twitter, Facebook, or other social media to post search and rescue information. The GPS locations of these social media posts can then be used to create real-time crisis maps, which can help inform rescue personnel which areas to concentrate on. Lack of coordination among organizations from both inside and outside the locale might also occur, and this can waste valuable time – for example, by searching the same place several times for victims. To address this problem, large-scale disasters need an operations office to coordinate the rescue teams. An example of the challenges of search and rescue during the response to Hurricane Katrina is shown in Box 2, taken directly from the White House archives.

{kind=link}

Box 2: Search and rescue in the Hurricane Katrina disaster

-

Critical Challenge: Search and Rescue

After Hurricane Katrina made landfall, rising floodwaters in New Orleans stranded thousands on rooftops, requiring a massive civil search and rescue operation. The Coast Guard, FEMA Urban Search and Rescue (US&R) Task Forces, and DOD forces, in concert with State and local emergency responders from across the country, courageously combined to rescue tens of thousands of people. With extraordinary ingenuity and tenacity, Federal, State, and local emergency responders plucked people from rooftops while avoiding urban hazards not normally encountered during a waterborne rescue.

Yet many of these courageous lifesavers were put at unnecessary risk by a structure that failed to support them effectively. The overall search and rescue effort demonstrated the need for greater coordination between US&R, the Coast Guard, and military responders who, because of their very different missions, train and operate in very different ways. For example, Urban Search and Rescue (US&R) teams had a particularly challenging situation since they are neither trained nor equipped to perform water rescue. Thus, they could not immediately rescue people trapped by the floodwaters.

Furthermore, lacking an integrated search and rescue incident command, the various agencies were unable to effectively coordinate their operations. This meant that multiple rescue teams were sent to the same areas while leaving others uncovered. When successful rescues were made, there was no formal direction on where to take those rescued. Too often, rescuers had to leave victims at drop-off points and landing zones that had insufficient logistics, medical, and communications resources, such as atop the I-10 cloverleaf near the Superdome.

-

Lessons Learned

The Department of Homeland Security should lead an interagency review of current policies and procedures to ensure the effective integration of all Federal search and rescue assets during disaster response.

Credit: Whitehouse Archives [42]

As the tsunami or storm surge disaster unfolds, emergency workers need to help make sure survivors have access to water, food, shelter, medical care, and sanitation. Depending on the scale and location of the disaster, each of these needs may present significant logistical challenges. People displaced from their homes have no access to these essential needs, and even families whose homes were not destroyed may not have water (due to contamination or pipeline disruption) or food (due to supply chain interruption and loss of refrigeration from electricity outages). The number of injured may exceed the capacity of existing medical care facilities, and those facilities themselves may be damaged, destroyed, or without power in the wake of a tsunami or storm surge. Damage to water and sewage infrastructure may also create a risk of outbreaks of diseases such as cholera, which emphasizes the need for repairing critical infrastructure as quickly as possible.

{kind=link}

Response Examples from 2020: Hurricane Laura in S.W. Louisiana

Response Examples from 2020: Hurricane Laura in S.W. Louisiana

In the early hours of August 27, 2020, Hurricane Laura made landfall as a category 4 storm on the coast of Southwestern Louisiana, near the Texas border. This coastal area is sparsely populated, with the town of Cameron (population around 400) close to the shoreline and in the direct path. The industrial city of Lake Charles (population 80,000+) sits just 30 miles inland across flat, marshy terrain with direct water connections to the Gulf. Laura hit Lake Charles almost directly, packing winds of close to 150 miles per hour and leaving a path of destruction. Lake Charles and neighboring Westlake are home to several oil refineries and chemical plants. Oil refineries must be shut down with the approach of a storm to prevent hazardous results such as explosions, fires, and leaks. A chlorine manufacturing plant did catch fire and leak gases into the air. Laura’s storm surge was predicted to be up to 20 feet, and the warnings used words like “unsurvivable” to try to convince coastal residents to heed the evacuation warnings. It appears that: 1. Most residents did heed the warnings, and 2. Laura’s measured surge did not reach the predicted height at landfall.

NOAA’s water level gauges available on the site: NOAA Tides and Currents - Inundation Dashboard [44]registered close to 10 feet at Calcasieu Pass. There were no operable gauges immediately east 0f the Calcasieu Pass gauge, so the actual maximum storm surge will be determined by analyzing high-water marks using field methods. This will probably reveal higher water levels to the east of the eye of the hurricane. There have been no drowning deaths reported to date, although 14 deaths have been attributed to Laura, with 8 of those due to carbon monoxide poisoning when gas-powered electrical generators were used in closed spaces. An additional 4 deaths were attributed to falling trees. There is no doubt that it could have been worse, but many harrowing tales are emerging. Perhaps the most vivid have been told by the fishermen who stayed with their boats sheltering in the bayous near Lake Charles, connected to Calcasieu Pass. These seasoned watermen feared for their lives and helped each other survive as they watched boats come apart and sink, even as they sat in port. Amazingly, everyone survived. Meanwhile, thousands of families evacuated ahead of the storm, heeding the mandatory evacuation orders.

Due to the COVID-19 pandemic, which has hit Louisiana hard, the state provided a system by which evacuees were provided shelter in hotel rooms, rather than congregate settings of traditional shelters. Baton Rouge and New Orleans were the two main destinations. In New Orleans, evacuees, some arriving by state-chartered buses, and others in private vehicles, had to register at a central location before being assigned a room. Phone and text numbers were made available to obtain information. Electronic message boards on the I-10 entering New Orleans displayed a number to call for assistance. By Monday after Hurricane Laura’s Thursday landfall, all rooms were filled, with more than the 9,000-person capacity in New Orleans having been reached. Other people found shelter with relatives, friends, or found their own accommodation elsewhere.

It is worth noting here that Louisiana’s emergency planning and response has had plenty of practice in recent years. In our case studies, we look at the aftermath of Hurricane Katrina, almost exactly 15 years before Laura. In September 2005, Hurricane Rita also hit the same communities as Laura did 15 years later. Not only have the state, parish, and municipal government Emergency Operation Plans been refined and developed over these years, but the residents of coastal Louisiana have lots of experience in planning and response on a personal and family level. This does not diminish the trauma and hardship felt when displaced from your home, not knowing if it has been destroyed or not.

In addition to helping people get out of the way of a major hurricane, what does the immediate response look like when the state EOP is put into practice? The first step is to mobilize first responders from around the state to perform search and rescue in the affected communities. This includes many units, including fire-fighters, EMS and other medical personnel, and state agencies such as the Department of Wildlife and Fisheries, with boats, aircraft, and helicopters available. On a federal level, the National Guard and the Coast Guard are deployed. In addition, non-governmental organizations including the Red Cross are on the ground to distribute needed supplies to survivors.

Typically, the hurricane leaves large areas without power. This is highly predictable, so power companies deploy personnel before the storm makes landfall and stage thousands of trucks and linemen from within the state and neighboring states to secure electrical lines and begin repairing them as soon as the storm has passed. In addition, other infrastructure such as water supply and sewerage must be repaired before a community is livable again.

Private citizens also participate in the search and rescue operations, with Louisiana’s fleet of private boats pressed into service by the now-famous “Cajun Navy”, who made their debut in 2016 after the devastating floods in Baton Rouge and assisted in Houston after Hurricane Harvey’s floods in 2017. Private citizens can also help by making donations of needed items and money to charities assisting those affected by the storm. The importance of charitable and non-profit organizations at these times cannot be overstated, as it takes time for government funds and relief to be released.

Cultural Norms and Religious Laws

Cultural Norms and Religious Laws

As in the preparedness phase of the emergency management cycle, emergency managers, rescue team members, and medical service providers must be sensitive to the cultural norms and religious laws of the victims to avoid adding further stress during disaster response. For instance, some cultures require unmarried men and women to live separately, so disaster emergency staff could create significant trauma by asking men and women to stay in the same quarters. Emergency workers could also cause stress if they provided pork products to strict Muslim or Orthodox Jewish victims, whose religions strictly forbid the consumption of pork. Racial and ethnic issues might also come into play during disaster response. Emergency shelters also need to be sensitive when sheltering people of different races and ethnicities. In these and other potentially difficult cultural and social circumstances, emergency managers, staff, and volunteers must be ready to coordinate among people with varying backgrounds, needs, and expectations.

Summary: Response

Summary: Response

In sum, all disaster responses require coordination, cooperation, and cultural sensitivity, but the complexity of, and challenges presented by, the response effort increases significantly with the size of the disaster. The case of the 2004 Indian Ocean tsunami – one of the greatest disasters of all time, with an enormous, unprecedented response required of the international community to address a disaster that affected numerous developing countries with varying languages, cultures, religions, and levels of development – demonstrates this complexity. Emergency response policies at all scales need to recognize and account for complexity.

Recovery

Recovery

In the recovery phase of the emergency management cycle, policymakers aim to repair, reconstruct, and restore what has been lost during a disaster. Recovery policies and activities also ideally aim to reduce future vulnerability to natural hazards, so that renewal might result in a physical and socio-economic environment that looks and functions somewhat different when compared to the original community. This is where recovery and mitigation may overlap in the cycle. During recovery, for example, city planning experts may call for rethinking how a community wiped out by a storm surge or tsunami is designed so that it has greater resilience than the original. Rebuilding employing methods designed so that the buildings can better withstand a storm surge – such as elevating the buildings above base flood elevation - would be the simplest example. Moving buildings to a safer location is also an option. There are many other details and considerations that can be incorporated, some of which were discussed in the Managed Retreat and Smart Building modules of the course. Consensus is recently being reached that building back communities exactly as they were is not the wisest path to take.

Funding Recovery

Funding Recovery

Effective recovery requires financial resources, usually in the form of cash or loans. Cash can come from a variety of sources, depending on the context and circumstances of a particular disaster. The local and national governments of affected countries are typically the first source of funds. In some countries, including the U.S., there are funds reserved for disasters but – particularly in poorer countries – funding available from these sources may be insufficient to cover a large disaster or multiple smaller disasters.

Donations of various kinds are a second major source of funds, particularly in major international disasters, such as the 2004 Indian Ocean tsunami or the 2011 Tohoku earthquake and tsunami in Japan. Donations can come from other governments (as in the case of the United States Agency for International Development’s efforts in countries affected by the Indian Ocean tsunami), from non-profit, non-governmental organizations like the International Red Cross/Red Crescent, from direct donations by private citizens and businesses, and from various other sources. Insurance payouts are a third source of funding for recovery.

Individuals and businesses in developed countries are often required by governments and lenders to carry insurance, but insurance is far less common in developing countries. In those countries, loans typically make up the remainder of recovery funds. These loans are often offered by major international financial institutions, particularly the World Bank and the International Monetary Fund. Such loans are sometimes controversial because they usually come with political and economic strings attached that policymakers and citizens of recipient countries dislike. These lending institutions played a major role in financing recovery in nations affected by the Indian Ocean tsunami. In summary, internal government transfers, donations, insurance, and loans typically provide local governments, institutions, emergency managers, and private citizens with needed financial resources to pay for recovery.

Reconstruction of Basic Infrastructure and Buildings

Reconstruction of Basic Infrastructure and Buildings

Tsunamis and storm surges are tremendously destructive to the built environment of coastal communities, and the aftermath is overwhelming as houses and businesses are wrecked and infrastructure is crippled. Restoring basic infrastructure is the first line of business after the water recedes. This includes restoring water, sewerage, roads, electricity, and telecommunications. The funds come from a combination of local government funds, utility company coffers, and state and national government aid. Local government funds rely on property and business tax receipts, but if much of the tax base has been destroyed in the disaster, then sufficient local funds for rebuilding infrastructure cannot be sustained. Consequently, in most cases, funds for the reconstruction of water, sewer, and roads must come from state and national government aid.

The task of rebuilding homes and businesses – all the buildings damaged by the event also must be funded and typically, building reconstruction is funded with a combination of insurance payouts, government aid, and other funds from private and non-profit sources. For private homeowners, this is a very stressful and often expensive process and can take a great deal of time, during which your family may need to be living elsewhere. As we have noted in Module 11, it is a process that proves much easier for people with strong economical means and can be very hard for people who have few resources.

Ideally, rebuilding should not be done in a business-as-usual way, using the same locations and with construction techniques led to damage in the initial disaster. However, meeting higher standards and building in a different, safer location can be expensive. Following a hurricane disaster in the United States, insurance payouts and government aid are contingent on rebuilding houses with hurricane-resistant designs to reduce future hurricane risk. This can include elevating the house to a new level required for insurance coverage and using materials and methods that make the building more resistant to hurricane damage.

After Hurricanes Katrina and Rita in Louisiana in 2005 many homeowners were unable to rebuild to the new standards and had to move to different communities further inland. Communities such as Cameron, Louisiana, which was devastated by Hurricane Laura in 2020 had only 400 residents at the time. The census data show that Cameron’s population diminished by 79% between the years 2000 and 2010 during which it was impacted by Hurricanes Rita and Ike. Another phenomenon is the change in demographics in certain communities over time after multiple storms impact them. For example, Grand Isle, Louisiana, Dauphin Island, Alabama, and other barrier island and beach communities which were home to modest fishing camps and year-round housing prior to the multiple storm events that have occurred over the past few decades, now boast many more very large, expensive structures belonging to wealthy business-people or corporations. They are now often rented for short-term vacations. This trend has changed who can enjoy coastal areas.

The photo below shows a typical elevated, storm surge-resistant house in Charleston, South Carolina. The first floor of the house is designed not for living, but instead for parking, storage, and building access. Special construction designs, like elevated slab and elevated crawlspaces, and use of non-water-sensitive materials, are also important. Eventually, all buildings in storm surge-prone locations of the United States will be replaced by similar surge-resistant designs.

The Complex Nature of Community Recovery

The Complex Nature of Community Recovery

There are many other aspects of recovery besides the reconstruction of infrastructure and buildings. Economic recovery is obviously vital because a strong local economy can help residents recover more quickly than a weak economy. At the same time, social and psychological recovery must be emphasized and not overlooked. Every aspect of peoples’ lives are disrupted by disaster, and many people suffer from psychological issues such as PTSD in post-disaster situations. The stress of the recovery process, including financial strain, separation of families, and other stressors can have very negative effects on a community.

Environmental recovery is also fundamental because the natural environment provides essential ecosystem services, so recovery cannot be complete without a healthy environment. Storm surge can cause severe environmental damage as many spills occur as a result, including overflows of sewerage treatment plants, oil and gas storage facilities, and wells, among others. After Katrina, whole neighborhoods near New Orleans were contaminated with petroleum from a refinery. These types of environmental impacts take a great deal of time to resolve. Additionally, agriculture and fisheries in an area impacted by a storm surge or tsunami can be devastated.

The combination of infrastructure, building, economic, environmental, and social recovery demands input from many stakeholders. For example, building recovery plans require input from local planning departments, homeowner associations, contractors, utility companies, and many others. As a result, it is important to adopt policies that identify stakeholders in building recovery – as well as in economic recovery, environmental recovery, and socio-psychological recovery – and ask them to join with government actors to participate in creating a post-disaster recovery plan during the mitigation phase of the emergency management cycle.

Expanding on these ideas about recovery, a hurricane-related disaster can have tremendous impacts on a local economy. For example, although Hurricane Charley in 2004 brought no significant storm surge, the storm’s category 4 winds severely affected the City of Punta Gorda, Florida. Many of the buildings in the downtown area were destroyed. The unemployment rate for the city rose 2.2 percent in the following month, and it took more than a year for the unemployment rate to return to pre-disaster levels. Thus, coastal disasters are huge drains on local economies and – if the scale of the disaster is big enough, as in the cases of Hurricane Katrina and Superstorm Sandy – on national economies, at least in the short- to medium-term (see case studies).

In the business sector, industries that are affected by a coastal disaster are often specific to the country and locality, but typically include at least some combination of tourism, health care, agriculture, fishing, and manufacturing. In 2020, Hurricane Laura ruined sugar cane and rice crops, killed hundreds of cattle, and sank fishing boats in southwest Louisiana. Farmers and fishermen have a long road to recovery after these types of impacts.

Tsunamis, hurricane storm surge, and other coastal hazards can destroy important tourist and health care infrastructure, including hotels, restaurants, and eldercare facilities. Recovery of the tourism and healthcare sectors is a priority for many coastal local governments. The health care sector is particularly important in many coastal communities of the southern United States, which have a high proportion of elderly residents that have retired from colder climates to warmer beach communities.

Environmental Recovery

Environmental Recovery

The environment provides many services to humans and wildlife, and our lives are intricately linked with our environment. So, when a major disturbance to the environment occurs, such as a tsunami or storm surge, the natural environment – the natural ecosystems - in the affected area can be severely impacted, and the ecosystem services may be destroyed or disrupted. For tsunami and especially hurricane protection, coastal ecosystems like mangroves, barrier islands, wetlands, and coral reefs can absorb and reduce wave energy and water height, thereby protecting the land from erosion, but at the same time, they can sustain heavy damage from the energy of the water. For these and many other reasons, environmental recovery and restoration are important elements of disaster recovery. Some of the examples of environmental restoration after tsunami and storm surge disasters include beach and sand dune restoration, wetland restoration, and water and soil protection, and recovery. Other environmental recovery activities include the restoration of urban forests, habitat recovery for wildlife, and debris recycling.

![By Michael L. Bak [Public domain], via Wikimedia Commons](http://commons.wikimedia.org/wiki/File:Fishing_boats_in_Banda_Aceh_after_2004_tsunami_DD-SD-06-07375.JPEG){kind=link}

An example of the importance of coastal ecosystem services and the damage caused by hurricane storm surge can be found in Louisiana at the time of Hurricane Katrina. The US Geological Survey estimated that a loss of more than 200 square miles of coastal wetlands was attributed to Katrina’s storm surge in Louisiana, an area representing approximately eight times the annual land loss rate already taking place (remember a football field of land on the Mississippi delta disappears every 100 minutes, so this is a lot of land!). The protection and economic benefits afforded coastal communities in Louisiana by these fragile and rapidly declining ecosystems were already well documented and recognized by the state. Following Katrina’s devastation, the state stepped up its existing coastal restoration program, creating a new State Coastal Master Plan and a new state agency to oversee and monitor restoration activities. As a result of devoting a new level of human and monetary resources, today Louisiana is a world leader in the science and engineering of coastal restoration and protection.

Other forms of environmental damage that must be remediated after a disaster include spills and other kinds of pollution resulting from the destructive forces of tsunamis and storm surges. The article The Indian Ocean Tsunami and its Environmental Impacts [48] outlines environmental impacts from the 2004 tsunami.

Psychological and Social Recovery

Psychological and Social Recovery

Finally, recovery is not complete without psychological and social recovery. After a disaster, many people suffer from post-traumatic stress disorder or PTSD. Among other symptoms, people with disaster-related PTSD can relive the hazard event repeatedly, feel in danger constantly, have difficulty sleeping, and refuse to return to places associated with the disaster. Victims’ psychological well-being and social life can therefore be severely affected by PTSD. As a result, PTSD and other psychological conditions of victims must be addressed as part of recovery. Social recovery is critical, too. Loss of jobs can lead to migration away from a community, and deaths of key community figures can change social dynamics. Although there is little that responsible organizations can do to directly influence these outcomes, it is important to be aware of these impacts in recovery efforts. Cultural recovery efforts, such as the rebuilding of religious landmarks and institutions, also improve the overall recovery.

Summary: Recovery

Summary: Recovery

In conclusion, it is important to note that the recovery period provides governments and emergency managers with a special opportunity to develop a more disaster-resilient society. Many of the older buildings with dated building codes and outmoded infrastructure have been destroyed, and people have become more aware of the risks associated with natural hazards. Thus, policies that mitigate by updating building codes, replacing obsolete infrastructure, and developing hazard-conscious land-use plans in the recovery phase will face fewer obstacles. At the same time, families will be more willing to mitigate by purchasing insurance and engaging in household preparedness activities.

Learning Check Point

Learning Check Point

Please take a few minutes to think about what you just learned then answer the questions below.

Case Study: Sumatra and Thailand and the 2004 Tsunami

Case Study: Sumatra and Thailand and the 2004 Tsunami

The Importance of Tsunami Warning Systems and the challenges of warning communication.

Think back to the video you watched in Module 7 – which included scenes of the 2004 tsunami event in Indonesia. The beginning of the video focused on the Banda Aceh area of Sumatra, where fishing communities and small coastal cities were completely destroyed, and the end of the video featured the Phuket area, where more tourist beaches were affected.

Through your reading and watching the videos, you hopefully gained an idea of what it is like to be caught in a tsunami with no advanced warning, and how frantic the attempts to get out of the way must be. Imagine what it would be like to try to move small children, sick or elderly people out of the way of a tsunami with before the wave strikes and with no time to spare!

In Module 7, the events in Phuket, Thailand, are described, with tourists enjoying their vacation on the beach at Christmas 2004. Many are oblivious to the dangers of the approaching tsunami. What could have been done differently? If this were to happen again, would these communities be better informed and prepared?

In Module 7 we also mentioned that early warning systems are very tricky because of the challenges of getting the message out soon enough after the earthquake and before the tsunami waves arrive at a particular shoreline. For example, the towns on the west coast of Sumatra are so close to the Andaman fault that they had almost no time to react, so a warning may not have worked, regardless of how well it was transmitted. Banda Aceh, on the northern tip of Sumatra, was devastated in 2004 because people did not have time to react, while there is evidence that some small nearby island communities fared better where traditional knowledge of the natural warning signs such as the sudden receding of the tidal waters was employed, and residents were able to flee to higher ground. Meanwhile, the tourist destinations of Phuket and Phi Phi, and nearby locations in Thailand had 2 hours, but the warnings were lacking. Visitors lacked necessary knowledge of nature’s warning signs and how to react, and may not have felt the earthquake, so many lives were lost.