Lessons

This is the course outline.

Lesson 1: Investment Decision Making and Compound Interest

Introduction

Overview

This course deals with mineral and oil project evaluation and investment decision-making. We will start by introducing the process of investment decision-making and the compound interest rate method. To make an investment decision, one needs to experience the processes of defining the problem, analyzing the problem, developing alternative solutions, deciding upon the best solution and converting the decision into effective action.

Then, in Lesson 1, the compound interest rate will be covered. Using the compounding method, we can select the appropriate factors to calculate the future value, current value, and the annual value.

One goal of this course is the application of project evaluation methods in the mining and oil industry. Besides the evaluation techniques, this lesson will cover some background and knowledge about the mining and oil industries, through readings of news and papers.

Learning Objectives

At the successful completion of this lesson, students should:

- understand the processes of investment decision-making;

- understand how to use compounding interest rates to calculate present, future, and annual values;

- understand how to apply the evaluation techniques in the mining and oil industry; and

- understand how to use Microsoft Excel for the calculations.

What is due for Lesson 1?

| Reading | Chapter 1 of the textbook by Stermole. |

|---|---|

| Assignment |

Go through the Syllabus, Orientation, and Lesson 1 on the website. |

Questions?

If you have any questions, please post them to the discussion forum, located under the Modules tab in Canvas. The TA and I will check that discussion forum daily to respond. While you are there, feel free to post your own responses if you, too, are able to help out a classmate.

Introduction to Investment Analysis

Investors make decisions relying on the relative profit potential of investment alternatives. The wrong choices may be made if systematic and quantitative methods are not used. In a given investment situation, it is necessary to consider several economic and technical parameters with respect to costs, profits, savings, the choice of time, tax and loyalty, project life, etc. If a reliable approach is not used to quantify the effects of these factors, it is very difficult to correctly assess each alternative and make the best choice.

The economic viewpoint assumes that capital accumulation is the primary investment objective of capitalistic individuals, companies and societies. From the late 1980s to the late 1990s, it is estimated that more capital investment dollars were spent in the US than were spent cumulatively in the past 200 years in the US. And the numbers in the 2010s were even larger. The importance of proper economic evaluation techniques in determining the most economically-effective way to spend this money seems evident for individuals, companies, and societies. This course presents the development and application of these economic evaluation techniques.

Investment decisions are analyzed over the lifetime of a project which can be decades long, and there are many input data that are related to time such as escalation and inflation of costs and revenues. Therefore, predictions, forecasting, estimations, and assumptions are required for these data which is involved with risk and uncertainty. Consequently, results of the analysis are highly dependent on accuracy and correctness of the proposed inputs. However, the techniques provided in this text can give the decision maker much better ideas about the relative risks and uncertainties between alternatives. This information, along with the numerical economic evaluation results, can help the investors to make a better choice than without using them.

In the majority of cases, making business decisions means dealing with alternative choice problems, which includes selecting the best alternative from several possible choices. The economic evaluation techniques in this course are based on the premise that profit maximization is the investment objective; that is, the alternation that maximizes the future worth of available investment dollars. In general, this involves answering the question, “Is it better to invest cash in a given investment situation, or will the cash earn more if it is invested in an alternative situation?”

Several applicable and useful techniques for evaluating various investment situations will be covered in this course and include future, present, annual value, and break-even analysis. But, the course focuses mainly on methods such as compound interest rate of return (ROR) analysis, as the primary decision-making criterion used by the majority of firms and organizations, and net present value (NPV) analysis, as the second-most used technique, properly applied on an after-tax basis.

Taxes are a cost relevant to most evaluation situations and economic analysis must be done after-tax. This course will cover the scenarios that it is proper to neglect taxes such as government project evaluations where taxes do not apply. Also, the cases with taxes incorporated will also be discussed and analyzed.

There are two main categories of projects or investments that economic evaluation decision-making can be applied to:

- revenue producing investments

- service producing investments

A possible third classification, “saving producing projects” will be illustrated later in the course.

Discounting and Compounding

Compounding

In order to compare different alternatives in an economic evaluation, they should have the same base (equivalent base). Compound interest is a method that can help applying the time value of money. For example, assume you have 100 dollars now and you put it in a bank for interest rate of 3% per year. After one year, the bank will pay you . Then, you will put the 103 dollars in the bank again for another year. One year later, you will have . If you repeat this action over and over, you will have:

Which can be written as:

In general:

The value of money after nth period of time can be calculated as:

Which F is the future value of money, P is the money that you have at the present time, and i is the compound interest rate.

Example 1-1:

Assume you put 20,000 dollars (principal) in a bank for the interest rate of 4%. How much money will the bank give you after 10 years?

So the bank will pay you 29604.8 after 10 years.

Discounting

In economic evaluations, “discounted” is equivalent to “present value” or “present worth” of money. As you know, the value of money is dependent on time; you prefer to have 100 dollars now rather than five years from now, because with 100 dollars you can buy more things now than five years from now, and the value of 100 dollars in the future is equivalent to a lower present value. That's why when you take loan from the bank, the summation of all your installments will be higher than the loan that you take. In an investment project, flow of money can occur in different time intervals. In order to evaluate the project, time value of money should be taken into consideration, and values should have the same base. Otherwise, different alternatives can’t be compared.

Assume you temporarily worked in a project, and in the end (which is present time), you are offered to be paid 2000 dollars now or 2600 dollars 3 years from now. Which payment method will you chose?

In order to decide, you need to know how much is the value of 2600 dollars now, to be able to compare that with 2000 dollars. To calculate the present value of a money occurred in the future, you need to discount that to the present time and to do so, you need discount rate. Discount rate, i, is the rate that money is discounted over the time, the rate that time adds/drops value to the money per time period. It is the interest rate that brings future values into the present when considering the time value of money. Discount rate represents the rate of return on similar investments with the same level of risk.

So, if the discount rate is i=10% per year, it means the value of money that you have now is 10% higher next year. So, if you have P dollars money now, next year you will have and if you have F dollars money next year, your money is equivalent to dollars at present time.

Going back to the example, considering the discount rate of 10%:

We can calculate the present value of $2600 occurred 3 years from now by discounting it year by year back to the present time:

Value of 2600 dollars in the 2nd years from now

Value of 2600 dollars in the 1st years from now

Value of 2600 dollars at the present time

So, it seems at the discount rate of i=10%, present value of 2600 dollars in 3 years equals 1953.42 dollars, and you are better off, if you accept the 2000 dollars now.

With the following fundamental equation, present value of a single sum of money in any time in the future can be calculated. It means a single sum of money in the future can be converted to an equivalent present single sum of money, knowing the interest rate and the time. This is called discounting.

P: Present single sum of money.

F: A future single sum of money at some designated future date.

n: The number of periods in the project evaluation life (can be year, quarter or month).

i: The discount rate (interest rate).

Example 1-2:

Assuming the discount rate of 10 %, present value of 100 dollars which will be received in 5 years from now can be calculated as:

You can see how time and discount rate can affect the value of money in the future. 62.1 dollars is the equivalent present sum that has the same value of 100 dollars in five years under the discount rate of 10%

Note:

The concept of compounding and discounting are similar. Discounting brings a future sum of money to the present time using discount rate and compounding brings a present sum of money to future time.

Compound Interest Formulas I

Example 1-2 was about one single sum; what if you want to add some savings to your bank account each year? So, we need to learn some more techniques to be prepared for real-world economic evaluations. First, take a look at Figure 1-2. It can help us to better understand the investment evaluation problems.

| P | A | A | A | A | A | F | ||

|

|

||||||||

| 0 | 1 | 2 | 3 | ... | n-1 | n | ||

Figure 1-2: Time diagram

The horizontal line represents the time. The left-hand end shows the present time and the right-hand end shows the future. The numbers below the line (1, 2, 3, …, n) are time periods. Above each time period, there is a sum A, which shows the money that occurs in that time period; here, we assume all of them are equal payments, so:

A is a uniform series of equal payments at each compounding period;

P is a present single sum of money at the time zero;

F is a future sum of money at the end of period n. And i is the compound interest rate.

In order to understand an economic evaluation problem we have to determine:

- How much money is given?

- When is the money given (where on the timeline)?

- What is the time period (year, quarter, or month)?

- What is the interest rate?

- What needs to be calculated?

Following these steps, we just need to use the proper equation to solve the problem. Based on the unknown (asked) variable, there are six basic categories of problems here:

- F (future value) needs to be calculated from given P

- F (future value) needs to be calculated from given A

- P (present value) needs to be calculated from given F

- P (present value) needs to be calculated from given A

- A (uniform and equal period values) needs to be calculated from given F

- A (uniform and equal period values) needs to be calculated from given P

Table 1-1 displays a method of notation that can help summarize the given information and avoid confusion.

| To be Calculated Quantity | Given Quantity | Appropriate Factor (symbol) | Relationship | |

|---|---|---|---|---|

| 1 | F | P | ||

| 2 | P | F | ||

| 3 | F | A | ||

| 4 | A | F | ||

| 5 | P | A | ||

| 6 | A | P |

Note: “/” in the Appropriate Factor (symbol) column is not a division operator, the entire or , … is a factor (symbol). The first letter shows the variable that needs to be calculated and the second letter shows the given variable. The two subscripts on each factor are the given period interest rate, i, followed by the number of interest compounding periods, n.

The new notation helps us summarize the problem. The factor actually give a gives us a coefficient that when multiplied by given parameter, gives the unknown parameter.

All time value of money calculations involves writing an equation or equations to calculate F, P, or A. Each of terms in the column “Appropriate Factor (symbol)” has a name that you will learn later in this course.

Please watch the following (4:32) video:

1. Single Payment Compound-Amount Factor

The first category of six categories that were introduced explains the situation that the present value of money is given and asks you to calculate the future value according to the given interest rate of i per period and n period from now. This problem can be summarized with the factor (symbol) of and can be shown as:

| P | _ | _ | _ | _ | _ | F=? | ||

|

|

||||||||

| 0 | 1 | 2 | 3 | ... | n-1 | n | ||

Figure 1-3: Single Payment Compound-Amount Factor, F/Pi,n

As explained earlier, the future value of money after n period with an interest rate of i can be calculated using the Equation 1-1: which can also be written regarding Table 1-1 notation as: . The mathematical expression is called the “single payment compound-amount factor."

Compound Interest Formulas II

3. Uniform Series Compound-Amount Factor

The third category of problems in Table 1-5 demonstrates the situation that equal amounts of money, A, are invested at each time period for n number of time periods at interest rate of i (given information are A, n, and i) and the future worth (value) of those amounts needs to be calculated. This set of problems can be noted as . The following graph shows the amount occurred. Think of it as this example: you are able to deposit A dollars every year (at the end of the year, starting from year 1) in an imaginary bank account that gives you i percent interest and you can repeat this for n years (depositing A dollars at the end of the year). You want to know how much you will have at the end of year nth.

| 0 | A | A | A | A | F=? | ||

|

|

|||||||

| 0 | 1 | 2 | ... | n-1 | n | ||

Figure 1-4: Uniform Series Compound-Amount Factor,

In this case, utilizing Equation 1-2 can help us calculate the future value of each single investment and then the cumulative future worth of these equal investments.

Future value of first investment occurred at time period 1 equals

Note that first investment occurred in time period 1 (one period after present time) so it is n-1 periods before the nth period and then the power is n-1.

And similarly:

Future value of second investment occurred at time period 2:

Future value of third investment occurred at time period 3:

Future value of last investment occurred at time period n:

Note that the last payment occurs at the same time as F.

So, the summation of all future values is

By multiplying both sides by (1+i), we will have

By subtracting first equation from second one, we will have

which becomes:

then

Therefore, Equation 1-3 can determine the future value of uniform series of equal investments as . Which can also be written regarding Table 1-5 notation as: . Then .

The factor is called “Uniform Series Compound-Amount Factor” and is designated by F/Ai,n. This factor is used to calculate a future single sum, “F”, that is equivalent to a uniform series of equal end of period payments, “A”.

Note that n is the number of time periods that equal series of payments occur.

Please review the following video, Uniform Series Compound-Amount Factor (3:42).

Example 1-3:

Assume you save 4000 dollars per year and deposit it at the end of the year in an imaginary saving account (or some other investment) that gives you 6% interest rate (per year compounded annually), for 20 years. How much money will you have at the end of the 20th year?

| 0 | $4000 | $4000 | $4000 | $4000 | F=? | ||

|

|

|||||||

| 0 | 1 | 2 | ... | 19 | 20 | ||

So

A =$4000

n =20

i =6%

F=?

Please note that n is the number of equal payments.

Using Equation 1-3, we will have

So, you will have 147,142.4 dollars at 20th year.

| Factor | Name | Formula | Requested variable | Given variables |

|---|---|---|---|---|

| F/Ai,n | Uniform Series Compound-Amount Factor | F: Future value of uniform series of equal investments | A: uniform series of equal investments n: number of time periods i: interest rate |

4. Sinking-Fund Deposit Factor

The fourth group in Table 1-5 is similar to the third group but instead of A as given and F as unknown parameters, F is given and A needs to be calculated. This group illustrates the set of problems that ask you to calculate uniform series of equal payments (or investment), A, to be invested for n number of time periods at interest rate of i and accumulated future value of all payments equal to F. Such problems can be noted as and are displayed in the following graph. Think of it as this example: you are planning to have F dollars in n years and there is a saving account that can give you i percent interest. You want to know how much you have to deposit every year (at the end of the year, starting from year 1) to be able to have F dollars after n years.

| 0 | A=? | A=? | A=? | A=? | F | ||

|

|

|||||||

| 0 | 1 | 2 | ... | n-1 | n | ||

Figure 1-5: Sinking-Fund Deposit Factor,

Equation 1-3 can be rewritten for A (as unknown) to solve these problems:

Equation 1-4 can determine uniform series of equal investments, A, given the cumulated future value, F, the number of the investment period, n, and interest rate i. Table 1-5 notes these problems as: . Then . The factor is called the “sinking-fund deposit factor”, and is designated by . The factor is used to calculate a uniform series of equal end-of-period payments, A, that are equivalent to a future sum F.

Note that n is the number of time periods that equal series of payments occur.

Please watch the following video, Sinking Fund Deposit Factor (4:42).

Example 1-4:

Referring to Example 1-3, assume you plan to have 200,000 dollars after 20 years, and you are offered an investment (imaginary saving account) that gives you 6% per year compound interest rate. How much money (equal payments) do you need to save each year and invest (deposit it to your account) in the end of each year?

| 0 | A=? | A=? | A=? | A=? | F=200,000 | ||

|

|

|||||||

| 0 | 1 | 2 | ... | 19 | 20 | ||

So

F=$200,000

n=20

i=6%

A=?

Using Equation 1-4, we will have

So, in order to have 200,000 dollars at 20th year, you have to invest 5,436.9 dollars in the end of each year for 20 years at annual compound interest rate of 6%.

| Factor | Name | Formula | Requested variable | Given variables |

|---|---|---|---|---|

| Sinking-Fund Deposit Factor | A: Uniform series of equal end-of-period payments | F: cumulated future value of investments n: number of time periods i: interest rate |

Note that

Compound Interest Formulas III

5. Uniform Series Present-Worth Factor

The fifth group in Table 1-5 covers a set of problems that uniform series of equal investments, A, occurred at the end of each time period for n number of periods at the compound interest rate of i. In this case, the cumulated present value of all investments, P, needs to be calculated. In summary, P is unknown and A, i, and n are given parameters. And the problem can be noted as and displayed as:

| P=? | A | A | A | A | 0 | ||

|

|

|||||||

| 0 | 1 | 2 | ... | n-1 | n | ||

Figure 1-6: Uniform Series Present-Worth Factor,

If we replace substitute F in Equation 1-3 from Equation 1-2, we will have the present value as:

then,

Equation 1-5 gives the cumulated present value, P, of all uniform series of equal investments, A, as . And also can be noted as: .The factor is called the “uniform series present-worth factor” and is designated by . This factor is used to calculate the present sum, P that is equivalent to a uniform of equal end of period payments, A. Then

Note that n is the number of time periods that equal series of payments occur.

Please review the following video, Uniform Series Present Worth Factor (Time 3:35).

Example 1-5:

Calculate the present value of 10 uniform investments of 2000 dollars to be invested at the end of each year for interest rate 12% per year compound annually.

| P=? | A=$2000 | A=$2000 | A=$2000 | A=$2000 | 0 | ||

|

|

|||||||

| 0 | 1 | 2 | ... | 9 | 10 | ||

So,

A =$2000

n =10

i =12%

P=?

Using Equation 1-5, we will have:

Note that we use the factor when we have equal series of payments. i is the interest rate and n is the number of equal payments. There is an important assumption here, the first payment has to start from year 1. In that case will return the equivalent present value of the equal payments.

Now let's consider the case that we have equal series of payments and the first payment doesn't start from year 1. In that case the factor will give us the equivalent single value of equal series of payments in the year before the first payment. However, we want the present value of them (at year 0). So, we need to multiply that with the factor and discount it to the present time (year 0).

Example:

| P=? | A=$2000 | A=$2000 | A=$2000 | 0 | |||

|

|

|||||||

| 0 | 1 | 2 | ... | 10 | 11 | ||

Note that there are 10 equal series of $2,000 payments. But the first payment is not in year 1. The factor returns the equivalent value of these 10 payments to the year before the first payment, which is year 1.

| P=? | $2000(P/A12%,10) | 0 | |||||

|

|

|||||||

| 0 | 1 | 2 | ... | 10 | 11 | ||

However, we want the present value. So, we need to discount the value by one year to have the present value of 10 equal payments.

| P=? | $2000(P/A12%,10)(P/F12%,1) | 0 | |||||

|

|

|||||||

| 0 | 1 | 2 | ... | 10 | 11 | ||

Example: Now consider the the following case that the first payment starts at year 3:

| P=? | A=$2000 | A=$2000 | A=$2000 | 0 | ||||

|

|

||||||||

| 0 | 1 | 2 | 3 | ... | 10 | 12 | ||

| Factor | Name | Formula | Requested variable | Given variables |

|---|---|---|---|---|

| Uniform Series Present-Worth Factor | P: Present value of uniform series of equal investments | A: uniform series of equal investments n: number of time periods i: interest rate |

6.Capital-Recovery Factor

The sixth group in Table 1-5 belongs to set of problems that A is unknown and P, i, and n are given parameters. In this category, uniform series of an equal sum, A, is invested at the end of each time period for n periods at the compound interest rate of i. In this case, the cumulated present value of all investments, P, is given and A needs to be calculated. It can be noted as .

| P | A=? | A=? | A=? | A=? | 0 | ||

|

|

|||||||

| 0 | 1 | 2 | ... | n-1 | n | ||

Figure 1-7: Capital-Recovery Factor,

Equation 1-5 can be rewritten for A (as unknown) to solve these problems:

Equation 1-6 determines the uniform series of equal investments, A, from cumulated present value, P, as . The factor is called the “capital-recovery factor” and is designated by A/Pi,n. This factor is used to calculate a uniform series of end of period payment, A that are equivalent to present single sum of money P.

Note that n is the number of time periods that equal series of payments occur.

Please watch the following video, Capital Recovery Factor (Time 3:37).

Example 1-6:

Calculate uniform series of equal investment for 5 years from present at an interest rate of 4% per year compound annually which are equivalent to 25,000 dollars today. (Assume you want to buy a car today for 25000 dollars and you can finance the car for 5 years with 4% of interest rate per year compound annually, how much you have to pay each year?)

| P=$25,000 | A=? | A=? | A=? | A=? | A=? | 0 | |

|

|

|||||||

| 0 | 1 | 2 | 3 | 4 | 5 | ||

Using Equation 1-6, we will have:

So, having $25,000 at the present time is equivalent to investing $5,615.68 each year (at the end of the year) for 5 years at annual compound interest rate of 4%.

| Factor | Name | Formula | Requested variable | Given variables |

|---|---|---|---|---|

| Capital-Recovery Factor | A: uniform series of equal investments | P: Present value of uniform series of equal investments n: number of time periods i: interest rate |

Note that

Using these six techniques, we can solve more complicated questions.

Example 1-7:

Assume a person invests 1000 dollars in the first year, 1500 dollars in the second year, 1800 dollars in the third year, 1200 dollars in the fourth year and 2000 dollars in the fifth year. At an interest rate of 8%:

1) Calculate time zero lump sum settlement “P”.

2) Calculate end of year five lump sum settlement “F”, that is equivalent to receiving the end of the period payments.

3) Calculate five uniform series of equal payments "A", starting at year one, that is equivalent to above values.

| P=? | 1000 | 1500 | 1800 | 1200 | 2000 | F=? | |

|

|

|||||||

| 0 | 1 | 2 | 3 | 4 | 5 | ||

1) Time zero lump sum settlement “P” equals the summation of present values:

2) End of year five lump sum settlement “F”, that is equivalent to receiving the end of the period payments equals the summation of future values:

Please note that in the factor subscript, n is the number of time period difference between F (the time that future value has to be calculated) and P(the time that the payment occurred). For example, 1800 payment occurs in year 3 but we need its future value in year 5 (2 year after) and time difference is 2 years. So, the proper factor would be: .

3) Uniform series of equal payments "A" can be calculated from either P or F :

or

Example 1-8: repeat your calculations for the following payments:

| P=? | 800 | 1000 | 1000 | 1600 | 1400 | F=? | |

|

|

|||||||

| 0 | 1 | 2 | 3 | 4 | 5 | ||

1) Time zero lump sum settlement “P” equals the summation of present values:

2) End of year five lump sum settlement “F”, that is equivalent to receiving the end of the period payments equals the summation of future values:

3) Uniform series of equal payments "A" can be calculated from either P or F:

or

Cash Flow

The first step in conducting an economic evaluation analysis is to understand the concept of “cash flow.” “Cash flow” represents the net inflow or outflow of money during a given period of time that can be month, quarter, or year. Cash flow can be reported as before-tax cash flow (BTCF) and after-tax cash flow (ATCF).

Operating Profit or EBITDA = Gross Revenue or Savings – Operating Expenses

Before tax Cash Flow = Operating Profit or EBITDA – Capital Expenditure

After tax Cash Flow = Before tax Cash Flow – Income Tax Expenditure

Which is formatted as:

Gross Revenue or Savings

– Operating Expenses

_____________________________

Operating Profit or EBITDA

– Capital Expenditure

_____________________________

Before tax Cash Flow

– Income Tax Expenditure

_____________________________

After tax Cash Flow

EBITDA : Earnings before interest, taxes, depreciation, and amortization

Example 1-9:

Assume an investment project for which you need to invest 20 and 15 million dollars in year 0 and year 1 (you can think of it as 20 million dollars now and 15 million dollars next year) to build a facility. In year 2, the plant will start producing and you can make revenue by selling the products. Each year, starting from year 2, operating costs and tax have to be paid. Project net cash flow can be calculated as:

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 | Year 7 | Year 8 | |

|---|---|---|---|---|---|---|---|---|---|

| Revenue | 18 | 20 | 22 | 24 | 26 | 28 | 30 | ||

| Operating Cost | -4 | -4 | -4 | -5 | -6 | -8 | -10 | ||

| Capital Cost | -20 | -15 | |||||||

| Tax Cost | -3 | -4 | -5 | -6 | -7 | -8 | -9 | ||

| Project Cash Flow | -20 | -15 | 11 | 12 | 13 | 13 | 13 | 12 | 11 |

Each column stands for a time period (that can be year, quarter, month, …) and each cell shows the inflow or outflow of money. Investment cash flow in any year represents the net difference between inflows of money from all sources, minus investment outflows of money from all sources. The cash flow for this project for all years is calculated in the last row.

As you can see, all the costs (Capital Cost, Operating Cost, Tax, ...) are entered with the negative sign in the table, and then summation of each column gives the net cash flow in that year. The negative cash flow incurred in years 0 and 1 will be paid off by positive cash flows in years 2 through 8.

Discounted Cash Flow (DCF)

If future cash flow is discounted, we can have cash flow in terms of present value, which is called discounted cash flow (DCF). As explained before, DCF considers the time value of money and applies it to the inflow and outflow of money occurred in the future. DCF is a tool that enables us to compare the future cash flow with the present value of money.

Different investment projects have different cash flows that happen in different time intervals in the future and DCF can give an assessment to decide which project is more profitable. DCF brings the future amounts to a same base that is easily understandable for decision makers. For example, assume you have two options: investing your money in Project A that gives you 1000 dollars every year from 2025 to 2035 or investing in Project B that gives you 1500 dollars every year from 2030 to 2040. Which project will you choose? DCF is a tool that can help you finding the answer. DCF can also be used to estimate the value of a company based on its future performance.

Example 1-10:

Please calculate the discounted cash flow from Example 1-9 assuming:

1) Discount rate = 10%

2) Discount rate = 12%

3) Discount rate = 15%

Assuming discount rate = 10%:

We can repeat the same procedure for discount rate = 12% and 15%. Table 1-2 shows the results.

| Year | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

|---|---|---|---|---|---|---|---|---|---|

| Project Cash Flow | -20 | -15 | 11 | 12 | 13 | 13 | 13 | 12 | 11 |

| DCF (discount rate = 10%) | -20 | -13.6 | 9.1 | 9.0 | 8.9 | 8.1 | 7.3 | 6.2 | 5.1 |

| DCF (discount rate = 12%) | -20 | -13.4 | 8.8 | 8.5 | 8.3 | 7.4 | 6.6 | 5.4 | 4.4 |

| DCF (discount rate = 15%) | -20 | -13 | 8.3 | 7.9 | 7.4 | 6.5 | 5.6 | 4.5 | 3.6 |

Net Present Value (NPV)

Now, all the DCFs in Table 1-3 have the same base, which is present value, consequently it’s possible to add them together and create a new criterion for project evaluation. The criterion which represents this summation is called net present value (NPV). NPV is the cumulative present worth of positive and negative investment cash flow using a specified rate to handle the time value of money.

Example 1-11:

Please calculate the NPV for the cash flow in Example 1-9 assuming:

1) Discount rate = 10%

2) Discount rate = 12%

3) Discount rate = 15%

Discount rate = 10%:

Assuming discount rate = 12%:

Assuming discount rate = 15%:

As you can see, the discount rate has a substantial effect on the project NPV, higher discount rates give lower NPV of the cash flow. The other important factor is the time. The closer the money is to present time, the higher present value it has, which affects the NPV.

Example 1-12:

Assume you have two alternative projects to invest your 600 dollars. The cash flow in Project A and Project B are shown in Table 1-4. Which project do you choose if the discount rate is 10%?

| Year | 0 | 1 | 2 | 3 |

|---|---|---|---|---|

| Project A Cash Flow | -600 | 500 | 300 | 200 |

| Project B Cash Flow | -600 | 200 | 300 | 500 |

Please note that two projects have similar numbers for cash flow but they happen in different times. DCFs are displayed in following table.

| Year | 0 | 1 | 2 | 3 |

|---|---|---|---|---|

| DCF for Project A | -600 | 454.5 | 247.9 | 150.3 |

| DCF for Project B | -600 | 181.8 | 247.9 | 375.7 |

This example shows how time affects the NPV of an investment project. As displayed in Table 1-5 and NPV calculations, Project A which has higher positive cash flows in closer time has higher NPV and it is a better alternative for investment than Project B.

Minimum Rate of Return

The terms “minimum rate of return," “hurdle rate," “discount rate," “minimum discount rate," and “opportunity cost of capital” are interchangeable with the term “cost of capital” as used in this course and in common practice. These terms should not be confused with the “financial cost of capital,” which is the cost of raising money by borrowing or issuing a bond, debenture, common stock or related debt/equity offerings. When the usual situation of capital rationing exists, the “opportunity cost of capital” generally is larger than the “financial cost of capital."

Microsoft Excel Tutorial

Microsoft Excel is a useful, convenient and widely used software for financial calculations and analysis that you will learn in this course. So, you are expected to learn and use required skills to utilize such tools.

If you do not have access to a commercial-grade spreadsheet program (such as Excel or OpenOffice), you can find free Spreadsheet applications available through Google Drive or a similar online tool. Following links include tutorials for Google Spreadsheet.

• Google Spreadsheet Tutorial from Google [1]

• Google Spreadsheet Tutorial from YouTube [2]

And also if you search online for “Google Spreadsheet Tutorial”, you can find some other good tutorial websites and videos.

Microsoft Excel

If it is the first time you are using Excel, please refer to the following video for a tutorial of Microsoft EXCEL 2010. (Time 10:00)

Please note that you need to open this video in YouTube [3]. (transcript [4])

You can follow the tutorial step by step to be a master of Excel 2010, which is a very powerful tool in the industry, business, and academia.

Tutorial for calculating present Value using Microsoft Excel (Time 7:35):

And also, these two following links (Times: 5:15 and 7:50):

Tutorial for calculating FutureValue using Microsoft Excel (Time 3:58):

For practice, I strongly recommend you to come back and solve the Lesson 1 examples in Excel and compare your results.

Summary of Lesson 1

Summary

Table 1-12 summarizes the material that we learned in Lesson 1.

| Factor | Name | Formula | Requested variable | Given variables |

|---|---|---|---|---|

| F/Pi,n | Single Payment Compound-Amount Factor | F: future value of a single sum | P: present single sum of money n: number of time periods i: interest rate |

|

| P/Fi,n | Single Payment Present-Worth Factor | P: equivalent present value of a single sum | F: single future sum of money n: number of time periods i: interest rate |

|

| F/Ai,n | Uniform Series Compound-Amount Factor | F: Future value of uniform series of equal investments | A: uniform series of equal investments n: number of time periods i: interest rate |

|

| A/Fi,n | Sinking-Fund Deposit Factor | A: Uniform series of equal end-of-period payments | F: cumulated future value of investments n: number of time periods i: interest rate |

|

| P/Ai,n | Uniform Series Present-Worth Factor | P: Present value of uniform series of equal investments | A: uniform series of equal investments n: number of time periods i: interest rate |

|

| A/Pi,n | Capital-Recovery Factor | A: uniform series of equal investments | P: Present value of uniform series of equal investments n: number of time periods i: interest rate |

To master all the knowledge to do your homework, you also need to go through the first two chapters of the textbook. Also, to finish your homework, you will need to know how to use Excel.

Reminder - Complete all of the Lesson 1 tasks!

You have reached the end of Lesson 1! Double-check the to-do list on the Lesson 1 Overview page [5] to make sure you have completed all of the activities listed there before you begin Lesson 2.

Lesson 2: Present, Annual and Future Value, and Rate of Return

Introduction

Overview

In this second lesson, we will enhance our knowledge of calculating present, annual, and future values, and then the rate of return analysis and break-even method will be explored. The calculation of present, annual, and future values is essential to project evaluation. And the rate of return and break-even methods are a critical framework to make investment decisions.Proper application of these different approaches to analyzing the relative economic merit of alternative projects depends on the type of projects being analyzed. As noted in Lesson 1, two basic classifications of investments are:

- revenue-producing investment alternatives

- service-producing investment alternatives

The application of these methods differs for revenue and service-producing projects. This lesson concentrates on the application of present worth, annual worth, future worth, and rate of return techniques and their examples. These methods are illustrated here on a before-tax analysis basis.

Learning Objectives

At the successful completion of this lesson, students should be able to:

- enhance their understanding of present, annual, and future values;

- understand the framework of break-even and rate of return analysis;

- use present, annual, and future values to make investment decisions; and

- use break-even and rate of return analysis to make investment decisions.

What is due for Lesson 2?

This lesson will take us one week to complete. Please refer to the Course Syllabus for specific timeframes and due dates. Specific directions for the assignment below can be found within this lesson.

| Reading | Go through the examples in Chapter 2 and 3 of the textbook for present, annual, and future values, as well as the examples of break-even and rate of return analysis. Sections include: 2.3, 2.4, 2.5, 2.6, 3.1, and 3.2. |

|---|---|

| Assignment | Homework 2. |

Questions?

If you have any questions, please post them to the discussion forum, located under the Modules tab in Canvas. I will check that discussion forum daily to respond. While you are there, feel free to post your own responses if you, too, are able to help out a classmate.

Nominal, Period, and Effective Interest Rates

Nominal, Period and Effective Interest Rates Based on Discrete Compounding of Interest

Usually, financial agencies report the interest rate on a nominal annual basis with a specified compounding period that shows the number of times interest is compounded per year. This is called simple interest, nominal interest, or annual interest rate. If the interest rate is compounded annually, it means interest is compounded once per year and you receive the interest at the end of the year. For example, if you deposit 100 dollars in a bank account with an annual interest rate of 6% compounded annually, you will receive dollars at the end of the year.

But, the compounding period can be smaller than a year (it can be quarterly, monthly, or daily). In that case, the interest rate would be compounded more than once a year. For example, if the financial agency reports quarterly compounding interest, it means interest will be compounded four times per year and you would receive the interest at the end of each quarter. If the interest is compounding monthly, then the interest is compounded 12 times per year and you would receive the interest at the end of the month.

For example: assume you deposit 100 dollars in a bank account and the bank pays you 6% interest compounded monthly. This means the nominal annual interest rate is 6%, interest is compounded each month (12 times per year) with the rate of 6/12 = 0.005 per month, and you receive the interest at the end of each month. In this case, at the end of the year, you will receive dollars, which is larger than if it is compounded once per year: dollars. Consequently, the more compounding periods per year, the greater total amount of interest paid.

Please watch the following video, Nominal and Period Interest Rates (Time 3:52).

Period interest rate i = r/m

Where m = number of compounding periods per year

r = nominal interest rate = mi

"An effective interest rate is the interest rate that when applied once per year to a principal sum will give the same amount of interest equal to a nominal rate of r percent per year compounded m times per year. Annual Percentage Yield (APY) is the standard term used by the banking industry to identify an effective interest rate."

The future value, F1, of investing P at i% per period for m period after one year:

| P | _ | _ | _ | _ | _ | F1 = P(F/Pi,m) = P(1+i)m |

|

|

||||||

| 0 |

1 |

2 |

... |

m periods per year |

||

And if the effective interest rate, E, is applied once a year, then future value, F2, of investing P at E% per year:

| P | _ | _ | F2 = P(F/PE,1) = P(1+E)1 |

|||

|

|

||||||

| 0 | 1 period per year |

|||||

Then:

Since P the same in both sides:

Then:

If the effective Annual Interest, E, is known and equivalent period interest rate i is unknown, the equation 2-1 can be written as:

Going back to the previous example,

Please watch the following video, Effective Interest Rate (Time 4:02).

Example 2-1:

Assume an investment that pays you 2000 dollars in the end of the first, second, and third year for an annual interest rate of 12% compounded quarterly. Calculate the time zero present value and future value of these payments after three years.

| P=? | _ | _ | _ | _ | 2000 | _ | _ | _ | 2000 | _ | _ | _ | 2000 | F=? |

|

|

||||||||||||||

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | ||

Quarterly period interest rate i = 12/4 = 3%

Please note that since the interest rate is compounded quarterly, we have to structure the calculations in a quarterly base. So there will be 12 quarters (three years and 4 quarters per each year) on the time line.

The 2000 dollars interest is paid at the end of the first, second, and third year, which are going to be the last quarters of each year (4th quarter, 8th quarter, and 12th quarter).

Please watch the following video, Nominal and Period Interest Rates Example (Time 3:45).

Continuous Compounding of Interest

If an annual interest rate compounds annually, then it should be compounded once a year.

If an annual interest rate compounds semi-annual, then it should be compounded twice a year.

If an annual interest rate compounds quarterly, then it should be compounded 4 times per year.

If an annual interest rate compounds monthly, then it should be compounded 12 times per year.

If an annual interest rate compounds daily, then it should be compounded 365 times per year.

And if the compounding period becomes smaller, then the number of compoundings per year, m, becomes larger. In the limit as m goes to infinity, period interest, i, approaches zero. This case is called Continues Compounding of Interest. Using differential calculus, Continues Interest Single Discrete Payment Compound-Amount Factor (F/Pr,n) can be calculated as:

And, Continues Interest Single Discrete Payment Present Worth Factor (P/Fr,n)

r is nominal interest rate compounded continuously

n is number of discrete valuation periods

e is base of natural log (ln) = 2.7183

Example 2-2:

Lets recalculate example 2-1 considering continues compound interest rate of 12%:

Note: The following links explains how to use the excel function (EXP) to calculate e raised to the power of number:

Link 1: EXP Function in Excel [6]

Link 2: Excel Functions [7]

Please watch the following video, Continuous Compounding of Interest (Time 4:54).

“Flat” or “Add-on” Interest Rate

A flat or add-on interest rate is applied to the initial investment principal each interest compounding period. This means total interest received for the investment on a flat interest is calculated linearly and simply is the summation of interest on all periods. For example, if you invest 1000 dollars at the present time in a project with flat interest rate of 12% per annum for 100 days, you will receive 32.88 dollars after 100 days:

The flat interest rate is usually applied when interest is calculated for a portion of a year or period.

Note: In engineering economics, the term “simple interest” is usually used as “add-on” or “flat” interest rate as defined here.

Applications of Compound Interest Formulas

Example 2-3:

If an investment gives you 8% interest compounded annually, how long will it take to double your money, invested in present time?

By taking ln (natural log) or log from each side, we will have:

It takes 9 years to double your money for an investment with 8% interest compounded annually.

The following links show how to calculate natural log using Excel:

Link 1: LN Function [8]

Link 2: How to Return the Natural Logarithm of a Number using Formulas [9]

Example 2-4:

Calculate the present value of following payments assuming the interest rate of 10% (compounded per period)

| P=? | A2=1000 | A3=1000 | A4=1000 | A5=1000 | A6=1000 | ||

|

|

|||||||

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | |

Note that here, uniform series of $1000 start from year 2. However, factor returns the P in the year before beginning of the first payment, which is year 1 here. Therefore, to calculate the present value of these uniform series of payments, we need to discount that for one year by multiplying it by .

Example 2-5:

What is the present value and equivalent series of annual end-of-period values for payments occurred in the following timeline assuming the interest rate of 10% (compounded per period)?

| P=? | A1=1000 | A2=1000 | A3=1000 | A4=2000 | A5=2000 | A6=2000 | A7=3000 | A8=3000 | A9=3000 | |

|

|

||||||||||

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

Note that:

There are three equal series of 1000 dollars from year 1 to year 3 so the present value (at time 0) of those can be calculated as: .

There are three equal series of 2000 dollars from year 4 to year 6: Because gives the P of these three payments at the year 3 (one year before the first one) so we need to discount the value for three years to have the present value for time 0 so present value of three equal series of 2000 dollars from year 4 to year 6 equals:

There are three equal series of 3000 dollars from year 7 to year 9: and gives the P at the year 6 (one year before the first one) so we need to discount the value for six years to have the present value for time 0 so present value of three equal series of 3000 dollars from year 7 to year 9 equals:

Please watch the following video, Applications of Compound Interest Formulas (Time 4:56).

Note: As displayed in Figure 2-1, using Microsoft Excel, you can calculate all the present values and then add them together much more conveniently.

Example 2-6:

Assume you can invest in a machine that can yield the income after all expense of 1000 dollars twice in the first and second years, 2000 dollars twice in the third and fourth years, and 3000 dollars twice in the fifth and sixth years. At the end of the sixth year, the machine has a resale value of $10,000. How much can be paid for this machine at the present time with the interest rate of 10% compounded annually?

| P=? | A1=1000 | A2=1000 | A3=2000 | A4=2000 | A5=3000 | A6=3000 | F=10,000 | |

|

|

||||||||

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | ||

Here we have:

Two 1000 dollars at year 1 and 2, so the present value can be calculated as

Two 2000 dollars at year 3 and 4, so the present value can be calculated as . Because, similar to explanation in example 2-4 and 2-5, gives the present value of these two payments at the year 2 (one year before the first one) it needs to be discounted for two years to have the present value for time 0 and present value of two 2000 dollars at year 3 to year 4 equals 2000 .

Two 3000 dollars at year 5 and 6: similarly, PV of these two payments will be . Because returns the present value at year 4 and it is required to be discounted for 4 years to give the present value of these payments at time zero.

Figure 2-2 displays how you can calculate the present value in Microsoft Excel by adding up all the present values of payments occurring in different time periods.

Example 2-7:

In order to pay off a 100,000 dollars mortgage in 20 years with interest rate of 8% per year (compounded annually), how much will the annual end-of-year mortgage payments be?

| P=100,000 | A=? | A=? | A=? | A=? | |||

|

|

|||||||

| 0 | 1 | 2 | 3 | ... | 20 | ||

Break-Even Calculations

Similar to what we had in previous sections (such as Example 2-6), there are problems that require you to calculate present value (as an unknown variable) for payments occurring in the future as revenue, with interest rate or rate of return (as known variable). These types of calculations are called break-even and enable you to determine the initial investment cost that can break-even the future payments considering a specified interest rate. It gives you the equivalent amount of money that needs to be invested at present time for receiving the given payments in the future with the desired interest rate.

As explained in Lesson 1, time value of money affects present value calculations. Consequently, the size of the payments, interest rate, and also payment schedule are influential factors in determining present value and break-even calculations.

Example 2-8:

Assume two investments of A and B with the payment schedule as shown in Figure 2-3. Calculate the present value of these investments considering minimum rates of return of 10% and 20%. The calculation will give the initial cost that can be invested to break-even with 10% and 20% rate of return.

Please notice that cumulative payments for investment A and B are equal and the difference between two investments is in the payment schedule.

|

Investment A P=? |

A=100 | A=200 | A=300 | A=400 | |

|

|

|||||

| 0 | 1 | 2 | 3 | 4 | |

|

Investment B P=? |

A=400 | A=300 | A=200 | A=100 | |

|

|

|||||

| 0 | 1 | 2 | 3 | 4 | |

Figure 2-3a: In investment A, the payment (revenue) schedule will be 100, 200, 300, and 400 dollars at the end of the first, second, third and fourth year. In investment B, the payment (revenue) schedule will be 400, 300, 200, and 100 dollars at the end of the first, second, third and fourth year.

Assuming rate of return 10%:

Assuming rate of return 20%:

This example shows the effect of time on future payments.Cumulative payments for investment A and B are equal, and the difference between two investments is in the payment schedule. In investment B, the investor receives a larger amount of revenue in the closer future, which amortizes the investor’s principal more rapidly than “A."

Example 2-9:

Investing on an asset is expected to yield 2,000 dollars per year in income after all expenses for each of the next ten years. It is also expected to have a resale value of $25,000 in ten years. How much can be paid for this asset now if a 12% annual compound interest rate of return before taxes is desired? Note that the wording of this example can be changed to describe a mineral reserve, petroleum, chemical plant, pipeline, or other general investment, and the solution will be identical.

| C=? | I=2000 | I=2000 | I=2000 | ... | I=2000 | L=$25,000 | |

|

|

|||||||

| 0 | 1 | 2 | 3 | ... | 10 | ||

Figure 2-3b: Cash flow: 2,000 dollars per year in income after all expenses for 10 years and resale value of $25,000 in the tenth year.

C: Cost

I: Income

L: Salvage Value

Present Value Equation:

Let’s equate costs and income at the present time.

Present value of all costs =present value of all incomes plus present value of salvage

The result will be similar, if costs and revenue plus salvage is equated in any time.

Future Value Equation

If we equate costs and income by the end of the 10thyear, then:

future value of cost = future value of income + future value of salvage

Annual Value Equation

Let’s equate the annual value costs and incomes,

annual value of cost = annual value of income + annual value of return

Please note that an equation can be written to equate costs and incomes at any point in time and the same break-even initial cost of $19,350 can be obtained.

Rate of Return (ROR) Calculation

So far, we have learned how to determine the unknown variables including present value, future value, uniform series of equal investments, and so on. In these question types, the interest rate was a given parameter. But, there are situations where the interest rate,i, is the unknown variable. In such cases, we know (or expect) the amount of money to be invested and the revenue that will occur in each time period, and we are interested in determining the period interest rate that matches these numbers. This category of problems is called rate of return (ROR) calculation type. In these problems, we are interested to find the interest rate that yields a Net Present Value of zero (the break-even interest rate). This break-even rate is sometimes called the Internal Rate of Return.

For example, assume for an investment of 8000 dollars at present time, you will receive 2000 dollars annually in each of year one to year five. What would be the interest rate (compounded annually) for which this project would break even?

The problem can be written as:

or

With a trial and error procedure, we can find the interest rate that fits into this equation (i= 7.93%). Therefore, the rate of return on this investment (or Internal Rate of Return) is i= 7.93% per year.

Again, assume all the parameters are known and specified except the rate of return i. In order to determine i, usually, a trial and error method is used that will be explained in Example 2-10 and the following video.

Example 2-10:

In Example 2-9, assume 20,000 dollars is paid for the asset in present time (C = 20,000 dollars), a yield of 2,000 dollars per year in income after all expenses is expected for each of the next ten years and also the resale value in the tenth year will be 25,000 dollars. What annual compound interest rate, or return on investment dollars, will be received for this cash flow?

| C=20,000 | I=2000 | I=2000 | I=2000 | ... | I=2000 | L=$25,000 | |

|

|

|||||||

| 0 | 1 | 2 | 3 | ... | 10 | ||

Figure 2-4: Cash flow: 20,000 dollars investment at present time, 2,000 dollars per year in income after all expenses for 10 years and resale value of $25,000 in the tenth year.

An equation can be written setting costs equal to income at any point in time and the project rate of return i can be calculated, i.e., the beginning or end of any period. Here, we will use the present value method to determine internal rate of return, i.

In order to solve this problem, an equation that equates costs to income at any point in time (for example beginning or end of any period) should be written with the project rate of return i as an unknown variable.

present value equation at present time to calculate i:

It is very difficult to solve this explicitly for i. By trial and error, we can easily find the i that makes the right side of the equation equal to the left side.

For the initial guess of i=10% , the left side is:

And for i=12% , the left side is:

Then, we can try i=11% (the middle point) and i=11.5% to find 11.5% is the rate of return to make the left side to equal to the right side.

In Excel specifically, another way to calculate the break-even rate of return is to use the IRR function. As long as the project has an investment cost in the present year and subsequent cash flows, you can use the IRR function to calculate the Internal Rate of Return. (If the project has a different cost and cash flow structure, then it's harder to use the Excel function here.) This video [10] has a short example (without any narration) of the Excel IRR function. The Excel help file for IRR [11] is also very useful.

For an illustration of the trial and error method, see the following video, Trial and error problem in Excel (6:52).

(Please use 1080p HD resolution to view it).

Summary and Final Tasks

Summary

In Lesson 2 we have learned:

- nominal, period, and effective interest rates based on a discrete compounding of interest;

- present, annual, and future values and the conversions between the values as one of the most important fundamentals of the class; and

- how to conduct rate of return and break-even analysis, which are very critical frameworks for investment decision-making.

Reminder - Complete all of the Lesson 2 tasks!

You have reached the end of Lesson 2! Double-check the to-do list on the Lesson 2 Overview page [12] to make sure you have completed all of the activities listed there before you begin Lesson 3.

Lesson 3: Annual Percentage Rates, Salvage Value, Bond Investment and Financial Cost of Capital

Introduction

Overview

In Lesson 3, we will learn about Annual Percentage Rates (APR), Salvage Values, Bond Investments, Financial Costs, and Opportunity Costs of Capital. APR is another rate that is important to this class. Bond is a common investment tool these days. After this lesson, students will also be able to distinguish the financial cost of capital and the opportunity cost of capital. Similar to the previous lesson, the introduction in this class will be based on examples, textbook reading, and assigned reading materials.

Learning Objectives

At the successful completion of this lesson, students should be able to:

- understand Annual Percentage Rate and how to calculate it;

- evaluate the value of a bond and understand the cash flow pattern of a bond;

- demonstrate the concept of financial cost of capital and opportunity cost of capital; and

- evaluate a project(s) using Net Present Value, Benefit Cost Ratio, and Present Value Ratio.

What is due for Lesson 3?

This lesson will take us one week to complete. Please refer to the Course Syllabus for specific time frames and due dates. Specific directions for the assignment below can be found within this lesson.

| Reading | Read Chapter 3 of the textbook. |

|---|---|

| Assignment | Homework and Quiz 3. |

Questions?

If you have any questions, please post them on our discussion forum (not email), located under the Modules tab in Canvas. I will check that discussion forum daily to respond. While you are there, feel free to post your own responses if you, too, are able to help out a classmate.

Annual Percentage Rates (APR)

Annual Percentage Rate (APR) is usually used for loans, mortgages, and so on. APR represents an annualized expression of the cost of borrowing money.

When you take out a loan or mortgage on a property, in addition to the interest, you are required to pay some other transaction costs such as points*, loan origination fees, a home inspection fee, mortgage insurance premiums, … . Considering these costs, the amount of money that you will receive is actually somewhat less than what you requested. APR is the expression that reflects some of these costs, and under the Federal Truth in Lending Law, Regulation Z, the lender is required to provide this information to the borrower. Since APR includes mentioned transaction costs, it is higher than interest rates. You can think of APR as the rate of return on the loan taking process considering its costs.

* Loan points are a percentage of the loan value that is deducted as transaction cost.

APR can be a good tool for comparing different loans offered by lenders. But there are two issues that need to be considered before comparing APRs:

- how the lender calculates APR and what costs are included;

- the fact that the difference between APR and loan interest rate is higher for smaller loans with shorter lifetimes, considering similar costs.

For More information about APR please watch the video linked below.

Annual Percentage Rate Video (1:34) [13]

Example 3-1

Calculate the APR for a 5-year, $25,000 loan with the interest rate of 6% (compounded annually), considering 1.5 points and loan originating fee of 250 dollars. Assume all the costs are deducted at the time of taking the loan (present time).

Note: 1.5 points equals a cost of 1.5% of the loan value.

First, the uniform series of annual payments needs to be calculated.

Regarding Table 1-12 and Equation 1-6

Then, we have to calculate the costs and deduct them from the loan:

So, borrower will receive $24,375 at the present time and pay $5,934.91 to the bank, each year, starting from end of the year 1:

Now, we have to calculate the rate of return for such a project.

| Loan-cost= 24,375 | A=5,934.91 | A=5,934.91 | A=5,934.91 | A=5,934.91 | A=5,934.91 |

|

|

|||||

| 0 | 1 | 2 | 3 | 4 | 5 |

Present value of loan – present value of the costs = present value of all annual payments

With the trial and error technique, explained in the Lesson 2 section “Break-Even and Rate of Return (ROR) Calculations II,” we can calculate i =6.94% as the APR for loan.

Please watch the following video, Calculating APR for a loan or mortgage (4:43).

Excel formula to calculate Rate of Return

Rate of return for an investment can be determined by the try and error method that is previously explained. Also, a convenient way to learn to calculate rate of return is to use Microsoft Excel or Google Sheets and apply Internal a Rate of Return (IRR) function to the cash flow.

Note: You have to enter the occurred amounts in the spreadsheet in the form of cash flow (you can enter the years in horizontal or vertical direction). It means inflow and outflow of cash should be entered with different signs (depending on the project). So, you can enter the loan with negative signs at the present time and annual payments in following years with positive signs.

More information about the IRR function in provided in following links.

IRR Function in Microsoft Excel [14]

Excel ITT Function [15]

Please watch the following video, Internal Rate of Return (1:58).

Figure 3-1 displays the APR calculations for Example 3-1.

Bond Investment

Please read the materials and watch the videos in the following links:

Please Read the Material and Watch The Videos in These 2 Links

Investopedia Dictionary: Bond [16] (1:46).

Investopedia Dictionary: Bond Yield [17] (1:56).

Please watch the following video, Investing Basics: Bonds (3:56).

A bond is a financial tool that can help the government and corporations raise money for their investments. A bond is a document that simply means “I owe you” or “IOU.” The Government and corporations issue the bond for a specified period of time (can be weeks to years). Buyers pay the bond at face value (the price that is written on the bond) and purchase the bond once it is issued. In the end of the specified period (known as maturity date), buyers receive the face value. In return, bond issuers agree to pay a fixed annual amount as interest, called bond’s coupon. Some bonds allow the interest rate to be adjusted with inflation rate. And some bonds can be converted to common stock or other securities after a period of time. A good thing about a bond is that buyers don’t necessarily need to wait until the maturity date; they can sell their bonds before the maturity dates in the market. The price of a bond (a bond that is not new) depends on the financial market and interest rates in the market and can be higher or lower than its face value. If the interest rate in the market drops, then the bond can be sold at a higher price than the face value, and vice versa.

The organization that issues the bond usually backs (supports) it with some selected asset as collateral in case of bankruptcy. And if the issuer organization doesn’t provide real tangible assets for supporting the bond, the bond is called a “junk bond.” In general, bonds with a higher level of risk pay higher interest rates.

Brokers and investors usually measure economic performance in terms of compound interest rate of return, which is referred as “yield to maturity” (YTM), as well as the “current yield." Most bonds, debentures, and notes pay interest on a semi-annual basis, but related interest rates are described nominally. This means that the evaluation of a bond must be made on a semi-annual basis and then expressed as a nominal value.

The U.S. Government offers different types of securities [19] including:

- Treasury bills [20]

- Treasury notes [21]

- Treasury bonds [22]

- Treasury Inflation-Protected Securities (TIPS) [23]

- Floating Rate Notes (FRNs) [24]

Please read the materials provided in the above links.

If you would like to know more about the history of bonds and the bond market, you can find some interesting documentaries on YouTube.com.

Example 3-2

Calculate the rate of return for a new bond with a face value of $1000 dollars and a maturity date of 10 years that pays 30 dollars every six months.

| C = $1000 | I=$30 | I=$30 | I=$30 | L = $1000 | |

|

|

|||||

| 0 | 1 | 2 | ... | 20 | |

C: Cost

I: Interest Income (semi-annual)

L: Maturity Value

Present value of cost = present value of income

According to Table 1-12:

With the trial and error method, we can calculate that i = 3% per semi-annual period. So, the nominal rate of return equals 2*3 = 6% per year compounded semi-annually. In bond broker terminology, the term “yield to maturity” is used to describe this nominal rate of return and may be listed by acronym “YTM.”

The following figure shows how you can calculate rate of return using IRR function in Microsoft Excel. Please notice the figures and signs, especially the first and last years.

Old Bond Rate of Return Analysis

As explained before, buyers can sell their bonds in the market before their maturity dates.

Example 3-3

Assume person A buys the new bond that is explained in Example 3-2. After two years (in the end of the year), person A decides to sell the old bond to person B for 800 dollars. Calculate the rate of return of investment for person B.

Person B investment can be shown as:

| C = $800 | I=$30 | I=$30 | I=$30 | L = $1000 | |

|

|

|||||

| 0 | 1 | 2 | ... | 16 | |

We can write the equations for this investment as:

Present value of cost = present value of income

The trial and error technique or IRR function in Microsoft Excel gives that i = 4.82% per semi-annual period and a nominal rate of return 2*4.82 = 9.64%per year compounded semi-annually.

Note: the only thing different from previous the calculation is the time and investment cost.

Please watch the following video, Calculating return on a bond investment (7:53).

Example 3-4

Assume interest rates in the financial market dropped, which causes the price of an old bond to increase. So, person A in Example 3-2 can sell the old bond after two years (in the end of the year) to person B for 1200 dollars. Calculate the rate of return of investment for person B.

Similar to Example 3-3, person B's investment can be shown as:

| C = $1200 | I=$30 | I=$30 | I=$30 | L = $1000 | |

|

|

|||||

| 0 | 1 | 2 | ... | 16 | |

Present value of cost = present value of income

And rate of return per semi-annual period will be i = 1.58% and the nominal rate of return is: 2*1.58 = 3.16%per year compounded semi-annually.

Example 3-5

Now assume this situation: Since the interest rate dropped in the financial market, the issuer organization can call the old bonds after 4 years (from now -- total maturity period of 6 years). This means that at that time, the issuer organization takes the bond and pays the face value. Please calculate the rate of return for person B’s investment if he buys the old bond at $1200.

Person B's investment can be shown as:

| C = $1200 | I=$30 | I=$30 | I=$30 | L = $1000 | |

|

|

|||||

| 0 | 1 | 2 | ... | 8 | |

Note that the old bond will be called in 4 years from now after person B buys it.

Present value of cost = present value of income

The rate of return for person B’s investment will be i = 0.45% per semi-annual period and the nominal rate of return: 0.9% per year compounded semi-annually.

Financial Cost of Capital and Opportunity Cost of Capital

As briefly explained in the first lesson, the financial cost of capital for a project (for a privately owned company) can be the average cost of financing current projects (or under consideration projects). The opportunity cost of capital or minimum rate of return (denoted as “i*”) reflects other opportunities that exist for the investment of capital now and in the future. The opportunity cost of capital for an investment is higher and more important than the financial cost of capital. An investor will invest in a project only if the rate of return is higher than opportunity cost capital (minimum rate of return).

Rate of return is a decision method to accept or reject a project and it is not a reliable method to rank several projects in terms of investment. Also, the rate of return for a current project is not necessarily applicable to future projects. For example, if an investment project has the rate of return of 5%, but another investment with similar (or lower) risk (such as interest paid by the bank to the money in your account or interest from buying Treasury Bond) has the rate of return of 6%, then the minimum rate of return and opportunity cost of capital will be 6%, and the project is not acceptable for investment.

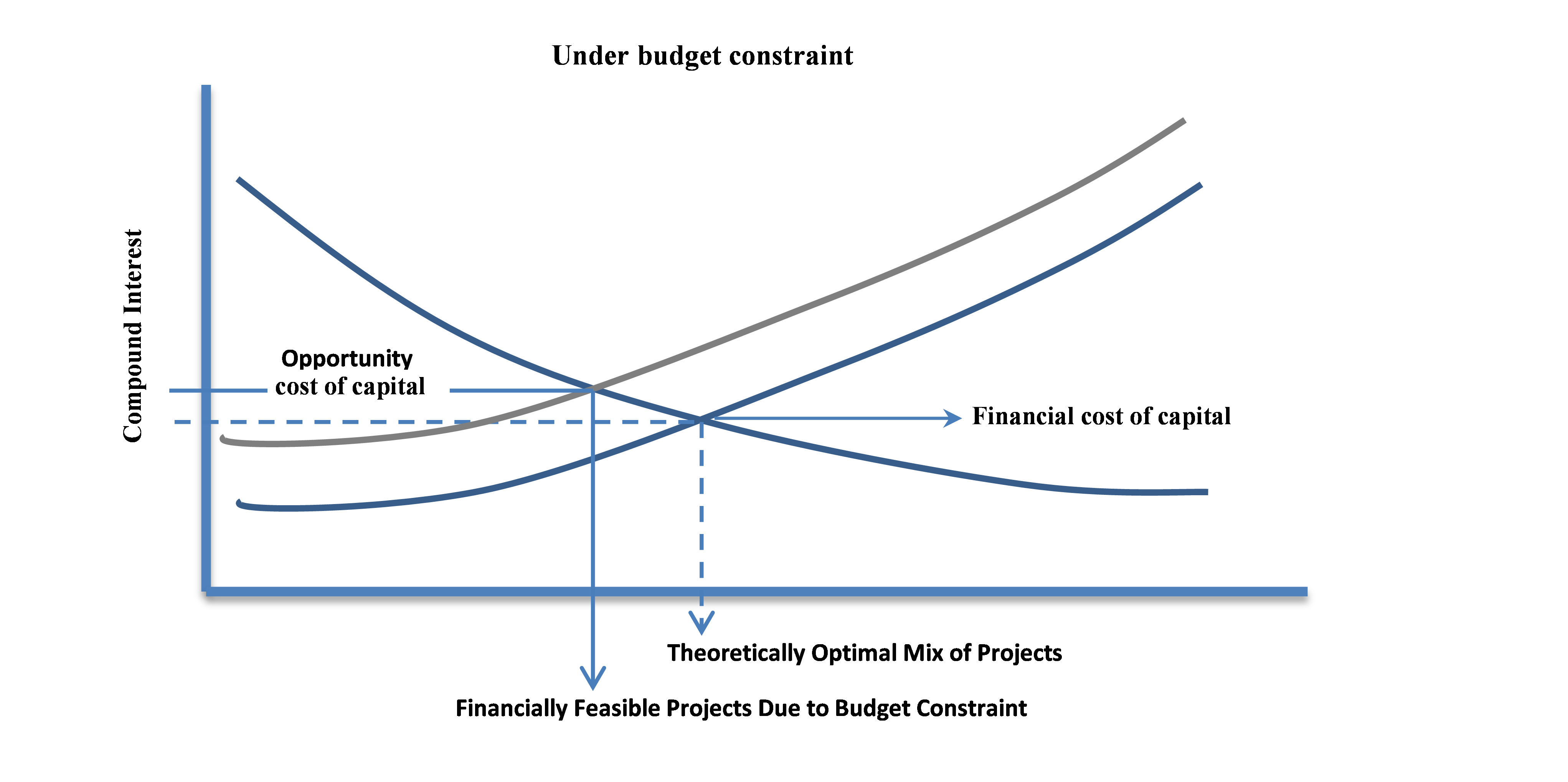

If a company doesn’t have budget constraints, then it would keep investing in a new project until the rate of return on the next project is less than the cost of raising money. See Figure 3-3, below.

But this assumption is not usually realistic, and in the real world, there is always a budget constraint. As Figure 3-4 shows, budget constraint causes the cost of the capital curve to move upward and also to the left. In this case, the financial cost of capital needs to be adjusted to a minimum acceptable rate of return (MARR). The minimum acceptable rate of return reflects the project’s rate of return that is given up for the project under consideration.

However, if the project that is under consideration is the only possible project or it is not comparable with other projects, or there is enough funding available for all other projects with a higher rate of returns, then the opportunity cost of capital can be equal to the financial cost of capital.

Net Present Value, Benefit Cost Ratio, and Present Value Ratio for project assessment

Net Present Value (NPV)

As explained in the first lesson, Net Present Value (NPV) is the cumulative present worth of positive and negative investment cash flow using a specified rate to handle the time value of money.

Or

Or

If the calculated NPV for a project is positive, then the project is satisfactory, and if NPV is negative then the project is not satisfactory.

The following video, NPV function in Excel, explains how NPV can be calculated using Microsoft Excel (8:04).

In the video NPV and IRR in Excel 2010 [25] (8:59) you can find another useful video for calculating NPV using Excel NPV function. In this video, cash flow is formatted in the vertical direction (there is absolutely no difference between vertical and horizontal formatting, using spreadsheet).

In the following video, IRR function in Excel, I'm explaining how to calculate the Rate of Return for a given cash flow using Microsoft Excel IRR function (4:19).

Example 3-6:

Please calculate the NPV for the following cash flow, considering minimum discount rate of 10% and 15%.

| C=60,000 | C=50,000 | I=24,000 | I=24,000 | ... | I=24,000 |

|

|

|||||

| 0 | 1 | 2 | 3 | ... | 10 |

C: Cost, I:Income

If using spreadsheet, following method can be more convenient:

Figure 3-5 illustrates the calculation of the NPV function in Microsoft Excel. Please note that in order to use the NPV function in Microsoft Excel, all costs have to be entered with negative signs.

Benefit Cost Ratio

Benefit Cost Ratio (B/C ratio) or Cost Benefit Ratio is another criteria for project investment and is defined as present value of net positive cash flow divided by net negative cash flow at i*.

For the project assessment:

- If B/C >1 then project(s) is economically satisfactory

- If B/C =1 then project(s) the economic breakeven of the project is similar to other projects (with same discount rate or rate of return)

- If B/C <1 then project(s) is not economically satisfactory

Present Value Ratio

Present Value Ratio (PVR) can also be used for economic assessment of project(s) and it can be determined as net present value divided by net negative cash flow at i*.

- If PVR>0 then project(s) is economically satisfactory

- If PVR=0 then project(s) is in an economic breakeven with other projects (with same discount rate or rate of return)

- If PVR<0 then project(s) is not economically satisfactory

Example 3-7

Calculate the B/C ratio and PVR for the cash flow in Example 3-6.

Figure 3-6 illustrates the calculation of the B/C function in Microsoft Excel. Please note that you need to use the absolute value in the denominator or multiply the answer by -1.

Figure 3-7 illustrates the calculation of the PVR function in Microsoft Excel. Please note that you need to use the absolute value in the denominator or multiply the answer by -1.

Summary and Final Tasks

Summary

In Lesson 3, we have learned that annual percentage rates (APR) represent an annualized expression of the cost of borrowing money, and how to calculate an APR based on a leader's cash flow. The salvage value is also introduced, which presents a positive cash flow for the project. Bonds are a very popular tool for corporations and governments to raise debt capital and we have learned the cash flows of a bond. The old bond rate or return with or without call privileges is also introduced. We also learned the concepts and effects of financial cost and opportunity cost of capital and in the last part we figured out how to evaluate a project(s) using Net Present Value, Benefit Cost Ratio, and Present Value Ratio.

Reminder - Complete all of the Lesson 3 tasks!

You have reached the end of Lesson 3! Double-check the to-do list on the Lesson 3 Overview page [26] to make sure you have completed all of the activities listed there before you begin Lesson 4.

Lesson 4: Mutually Exclusive Project Analysis

Introduction

Overview

Mutually exclusive projects: making an analysis of several alternatives from which only one can be selected, such as selecting the best way to provide service or to improve an existing operation or the best way to develop a new process, product, mining operation, or oil/gas reserve.

Non-mutually exclusive projects: analyzing several alternatives from which more than one can be selected depending on capital or budget restrictions, such as ranking research, development, and exploration projects to determine the best projects to fund with available dollars.

This lesson focuses on the analysis of mutually exclusive alternatives. Valid discounted cash flow criteria such as rate of return, net present value, and benefit-cost ratio are applied in very different ways in proper analysis of mutually exclusive and non-mutually exclusive alternative investments.

Learning Objectives

At the successful completion of this lesson, students should be able to:

- understand how to use rate of return and NPV analysis to evaluate mutually exclusive projects and non-mutually exclusive projects;

- understand how to conduct Incremental Analysis; and

- understand how variable minimum rate of return with time can affect the project.

What is due for Lesson 4?

This lesson will take us one week to complete. Please refer to the Course Syllabus for specific time frames and due dates. Specific directions for the assignment below can be found within this lesson.

| Reading | Read Chapter 4 of the textbook. |

|---|---|

| Assignment | Homework 4. |

Questions?